- 1-888-253-3960

- enquiry@vynzresearch.com

-

This is lorem ipsum doller

Emerging Infectious Disease Diagnostics Market

| Status : Published | Published On : Dec, 2023 | Report Code : VRHC1279 | Industry : Healthcare | Available Format :

|

Page : 220 |

Global Emerging Infectious Disease Diagnostics Market – Analysis and Forecast (2025-2030)

Industry Insight by Technology (polymerase chain reaction (PCR), isothermal nucleic acid amplification technology (INAAT), next-generation sequencing (NGS), immunodiagnostics, and other technologies), Type of Infection (bacterial, viral, fungal, and other infections), Disease Type (respiratory infections, sexually transmitted infections (STIs), gastrointestinal infections, and other infections), Application (laboratory testing and point-of-care testing), End-User (hospitals and clinics, diagnostics laboratories, and other end-users) and Geography (U.S., Canada, Germany, U.K., France, China, Japan, India, and Rest of the World)

Industry Overview

Emerging infectious disease diagnostics involves the identification and monitoring of novel pathogens that pose a threat to public health. Utilizing advanced technologies such as PCR, genomics, and immunodiagnostics, it aims to rapidly detect and characterize new infectious agents. This field plays a crucial role in outbreak response, enabling early containment measures and treatment strategies. Continuous surveillance, international collaboration, and the integration of artificial intelligence enhance the ability to swiftly diagnose and understand emerging diseases. By combining molecular biology with innovative diagnostic tools, Emerging Infectious Disease Diagnostics contributes to global efforts in preemptively managing and mitigating the impact of infectious threats on a population's well-being.

Global emerging infectious disease diagnostics market was worth USD 20.20 billion in 2023 and is expected reach USD 32.50 billion by 2030 with a CAGR of 6.44% during the forecast period, i.e., 2025-2030. The growing demand for emerging infectious disease diagnostics is driven by the increasing incidence of novel pathogens, rapid technological advancements in diagnostic tools, heightened awareness due to past pandemics, global surveillance efforts, and the imperative for prompt identification to facilitate timely public health responses.

Geographically, the global emerging infectious disease diagnostics market is expanding rapidly in North America, Europe, and the Asia Pacific, as a result of the robust healthcare infrastructure, advanced diagnostic technologies, proactive government initiatives, heightened awareness post-pandemics, and increasing research investments; however, the market confronts constraints such as regulatory hurdles, limited access to advanced diagnostic technologies in developing regions, resource constraints, and the unpredictable nature of emerging diseases. Overall, the emerging infectious disease diagnostics market offers potential prospects for market participants to develop and fulfill the growing needs of wide range of industries including hospitals and clinics, and diagnostics laboratories.

Emerging Infectious Disease Diagnostics Market Segmentation

Insight by Technology

Based on technology, the global emerging infectious disease diagnostics market is segmented into polymerase chain reaction (PCR), isothermal nucleic acid amplification technology (INAAT), next-generation sequencing (NGS), immunodiagnostics, and other technologies. Polymerase Chain Reaction (PCR) dominated the global emerging infectious disease diagnostics market in 2022 due to its precision, sensitivity, and rapid results. PCR enables targeted amplification of genetic material for specific pathogen detection. Examples include its pivotal role in diagnosing COVID-19, allowing rapid and accurate identification of the SARS-CoV-2 virus. While isothermal nucleic acid amplification technology (INAAT) offers simplicity, PCR's established track record and widespread adoption make it the current frontrunner. However, the landscape may evolve with ongoing advancements; for instance, Next-Generation Sequencing (NGS) is increasingly utilized for comprehensive genomic analysis in emerging infectious disease research.

Insight by Type of Infection

Based on type of infection, the global emerging infectious disease diagnostics market is segmented into bacterial, viral, fungal, and other infections. Viral infections currently dominate the global emerging infectious disease diagnostics market due to their propensity for rapid transmission and global impact. Notably, the rise of novel viruses, such as the COVID-19 in 2020 and the Zika virus, which emerged in 2015, and the ongoing challenges posed by influenza variants, underscores the need for effective viral diagnostics. These instances highlight the urgency and demand for diagnostics that can swiftly and accurately identify viral pathogens, shaping the market's focus towards viral detection technologies in the ongoing efforts to tackle emerging infectious diseases.

Insight by Disease Type

Based on disease type, the global emerging infectious disease diagnostics market is segmented into respiratory infections, sexually transmitted infections (STIs), gastrointestinal infections, and other infections. Respiratory infections currently dominate the global emerging infectious disease diagnostics market due to their widespread occurrence and significant public health impact. Notably, the COVID-19 pandemic, caused by the SARS-CoV-2 virus, has underscored the critical need for accurate and rapid respiratory diagnostics. With its unprecedented global impact since December 2019, COVID-19 has driven a surge in demand for respiratory diagnostics, emphasizing the urgency for effective tools in managing emerging infectious diseases. This trend is likely to persist as respiratory pathogens continue to pose substantial threats to public health worldwide.

Insight by Application

Based on application, the global emerging infectious disease diagnostics market is segmented into laboratory testing and point-of-care testing. Laboratory testing currently dominate the global emerging infectious disease diagnostics market due to its capacity for high-throughput, comprehensive analysis, and precise identification of pathogens. The significance of labs was evident during the COVID-19 pandemic, where central laboratories played a crucial role. For instance, the widespread use of RT-PCR tests, like the TaqPath COVID-19 Combo Kit, in labs facilitated large-scale testing since its FDA approval in July 2020. The extensive capabilities of labs, coupled with their infrastructure for complex testing procedures, make them essential in managing and understanding emerging infectious diseases, ensuring accurate diagnosis and facilitating effective public health responses.

Insight by End-User

Based on end-user, the global emerging infectious disease diagnostics market is segmented into hospitals and clinics, diagnostics laboratories, and other end-users. Hospitals and clinics dominated the global emerging infectious disease diagnostics market in 2023 due to their role as primary healthcare settings, where timely and accurate diagnostics are pivotal. The COVID-19 pandemic, exemplified by the rapid deployment of diagnostic tests in healthcare facilities globally, underscores this dominance. For instance, the widespread adoption of point-of-care PCR tests in hospitals, like the Xpert Xpress SARS-CoV-2 test, has enabled swift diagnosis since its FDA approval in March 2020. The centralization of diagnostic resources in hospitals and clinics ensures efficient patient management and containment of emerging infectious diseases, solidifying their position in the diagnostics market.

Global Emerging Infectious Disease Diagnostics Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2018 - 2023 |

|

Base Year Considered |

2024 |

|

Forecast Period |

2025 - 2030 |

|

Market Size in 2024 |

U.S.D. 20.20 Billion |

|

Revenue Forecast in 2030 |

U.S.D. 32.50 Billion |

|

Growth Rate |

6.44% |

|

Segments Covered in the Report |

By Technology, By Type of Infection, By Disease Type, By Application, By End-Use Industry |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Impact of COVID-19; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Middle East, and South America |

Industry Dynamics

Emerging Infectious Disease Diagnostics Market Growth Drivers

Continuous evolution of diagnostic technologies

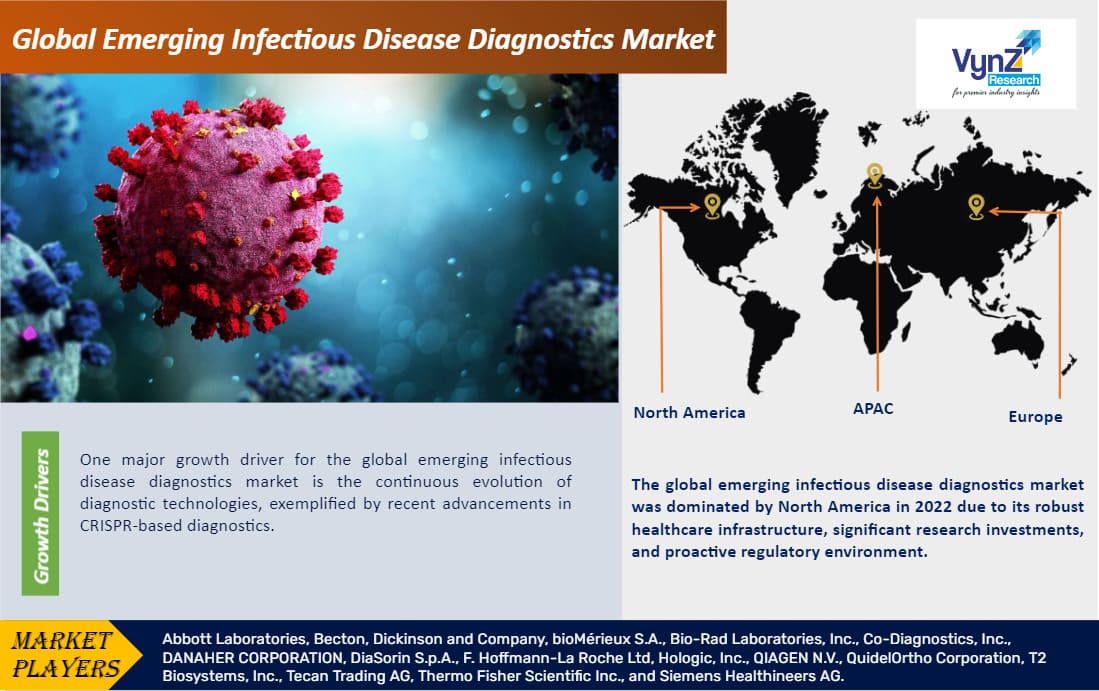

One major growth driver for the global emerging infectious disease diagnostics market is the continuous evolution of diagnostic technologies, exemplified by recent advancements in CRISPR-based diagnostics. In August 2021, the FDA granted Emergency Use Authorization for Sherlock BioSciences' Sherlock CRISPR SARS-CoV-2 kit, showcasing the potential of CRISPR technology in rapid and specific pathogen detection. CRISPR-based diagnostics offer advantages like high sensitivity, specificity, and potential for multiplexing, revolutionizing infectious disease diagnostics. The adaptability and precision of such technologies contribute significantly to the market's growth, fostering innovation in diagnostic approaches. As these technologies become more accessible and versatile, they are expected to reshape the landscape of emerging infectious disease diagnostics, driving market expansion and improving response capabilities in the face of novel pathogens.

Increasing emphasis on decentralized testing and point-of-care diagnostics

Another major growth driver for the global emerging infectious disease diagnostics market is the increasing emphasis on decentralized testing and point-of-care diagnostics. This shift is evident with the emergence of portable and rapid testing solutions, exemplified by the LumiraDx Platform. In October 2022, LumiraDx received FDA clearance for its SARS-CoV-2 Antigen Test on the LumiraDx Platform, showcasing the trend towards accessible and swift diagnostics. Point-of-care testing reduces turnaround time, enhances patient management, and aids in early containment efforts during outbreaks. The demand for user-friendly, on-site diagnostics, especially in resource-limited settings, is driving innovation in portable technologies, contributing significantly to market growth as healthcare systems globally prioritize decentralized testing for emerging infectious diseases.

Emerging Infectious Disease Diagnostics Market Challenge

Complex regulatory approval process

A major challenge for the global emerging infectious disease diagnostics market is the potential for regulatory complexities and delays in the approval process. Stringent regulatory requirements, varying across regions, can hinder the timely introduction of new diagnostic technologies. For instance, navigating the regulatory landscape for novel diagnostic tests, like those developed during public health emergencies, such as the COVID-19 pandemic, can be intricate. Delays in regulatory approvals may impede the rapid deployment of essential diagnostic tools, impacting the market's responsiveness to emerging infectious threats and hindering the ability to swiftly implement effective diagnostic solutions.

Emerging Infectious Disease Diagnostics Market Geographic Overview

-

North America

-

Europe

-

Asia Pacific (APAC)

-

Middle East and Africa (MEA)

-

South America

The global emerging infectious disease diagnostics market is segmented into North America, Europe, the Asia-Pacific, South America, and the Middle East and Africa region. The global emerging infectious disease diagnostics market was dominated by North America in 2023 due to its robust healthcare infrastructure, significant research investments, and proactive regulatory environment. Notably, the FDA's swift approvals of diagnostic tools during the COVID-19 pandemic, such as the FDA Emergency Use Authorization for Roche's Elecsys IL-6 test in June 2020, demonstrate the region's ability to efficiently respond to emerging threats. The concentration of major diagnostic companies, research facilities, and a well-established healthcare system enhances North America's position in driving innovation and rapid deployment of advanced diagnostics, consolidating its dominance in the global market.

Emerging Infectious Disease Diagnostics Market Competitive Insight

Abbott Laboratories is a leading player in the global emerging infectious disease diagnostics market, known for its innovative diagnostic solutions. Abbott's ID NOW COVID-19 test, granted Emergency Use Authorization by the FDA in March 2020, exemplifies their commitment to rapid and on-site testing. This molecular test provides results in just minutes, facilitating quick decision-making in healthcare settings. Abbott's global presence and extensive portfolio contribute to its dominance in infectious disease diagnostics, addressing challenges posed by emerging pathogens.

Bio-Rad Laboratories is a key player with a strong focus on infectious disease diagnostics. The company's Bio-Plex 2200 system offers multiplex testing capabilities, allowing simultaneous detection of various pathogens. This technology streamlines the diagnostic process, enhancing efficiency and accuracy. Bio-Rad's commitment to research and development is evident in their BioFire FilmArray system, which enables syndromic testing for a broad range of infectious diseases. These innovative solutions position Bio-Rad as a major influencer in the global emerging infectious disease diagnostics market, addressing the evolving landscape of infectious threats.

Recent Development by Key Players

UK-based Oxford Nanopore Technologies and Boston-based Day Zero Diagnostics announced partnership to develop a rapid diagnostic solution for bloodstream infections. The integrated system aims to provide same-day identification and genomic-based antibiotic susceptibility profiling without the need for blood culture. Leveraging Oxford Nanopore's high-throughput sequencing and Day Zero Diagnostics' AI-driven microbial identification technology, the collaboration seeks regulatory approvals, including from the U.S. FDA.

BD (Becton, Dickinson, and Company) - has launched the BD Vacutainer® UltraTouch™ Push Button Blood Collection Set in India to minimize patient pain and discomfort as well as enable single prick success during blood collection process.

Key Players Covered in the Report

Abbott Laboratories, Becton, Dickinson and Company, bioMérieux S.A., Zero Day Diagnostics, Bio-Rad Laboratories, Inc., Co-Diagnostics, Inc., DANAHER CORPORATION, DiaSorin S.p.A., F. Hoffmann-La Roche Ltd, Hologic, Inc., QIAGEN N.V., QuidelOrtho Corporation, T2 Biosystems, Inc., Tecan Trading AG, Thermo Fisher Scientific Inc., and Siemens Healthineers AG.

The emerging infectious disease diagnostics market report offers a comprehensive market segmentation analysis along with an estimation for the forecast period 2025–2030.

Segments Covered in the Report

-

By Technology

-

Polymerase Chain Reaction (PCR)

-

Isothermal Nucleic Acid Amplification Technology (INAAT)

-

Next-Generation Sequencing (NGS)

-

Immunodiagnostics

-

Other Technologies

-

By Type of Infection

-

Viral

-

Bacterial

-

Fungal

-

Others

-

By Disease Type

-

Respiratory Infections

-

Sexually Transmitted Infections (STIs)

-

Gastrointestinal Infections

-

Other Infections

-

By Application

-

Laboratory Testing

-

Point-of-Care Testing

-

End-User

-

Hospitals and Clinics

-

Diagnostics Laboratories

-

Other End-User

Region Covered in the Report

-

North America

-

U.S.

-

Canada

-

Mexico

-

Europe

-

Germany

-

U.K.

-

France

-

Italy

-

Spain

-

Russia

-

Rest of Europe

-

Asia-Pacific (APAC)

-

China

-

Japan

-

India

-

South Korea

-

Rest of Asia-Pacific

-

Middle East and Africa (MEA)

-

Saudi Arabia

-

U.A.E

-

South Africa

-

Rest of MEA

-

South America

-

Argentina

-

Brazil

-

Chile

-

Rest of South America

Primary Research Interviews Breakdown

%20System%20Market.png "Emerging Infectious Disease Diagnostics Market")

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By Vehicle Type

1.2.2. By Component

1.2.3. By Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1. Primary Research

1.5.1.2. Secondary Research

1.5.2. Methodology

1.5.2.1. Data Exploration

1.5.2.2. Forecast Parameters

1.5.2.3. Data Validation

1.5.2.4. Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2030

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. BEV

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2030

5.1.2. FCEV

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2030

5.1.3. PHEV

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2030

5.1.4. MHEV

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2030

5.2. By Component

5.2.1. Battery

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2030

5.2.2. Power Electronic Controller

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2030

5.2.3. Motor/Generator

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2030

5.2.4. Converter

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2030

5.2.5. Transmission

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2030

5.2.6. On-Board Charger

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2030

6. North America Market Estimate and Forecast

6.1. By Vehicle Type

6.2. By Component

6.3. By Country

6.3.1. U.S. Market Estimate and Forecast

6.3.2. Canada Market Estimate and Forecast

6.3.3. Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By Vehicle Type

7.2. By Component

7.3. By Country

7.3.1. Germany Market Estimate and Forecast

7.3.2. France Market Estimate and Forecast

7.3.3. U.K. Market Estimate and Forecast

7.3.4. Italy Market Estimate and Forecast

7.3.5. Spain Market Estimate and Forecast

7.3.6. Rest of Europe Market Estimate and Forecast

8. Asia-Pacific Market Estimate and Forecast

8.1. By Vehicle Type

8.2. By Component

8.3. By Country

8.3.1. China Market Estimate and Forecast

8.3.2. Japan Market Estimate and Forecast

8.3.3. India Market Estimate and Forecast

8.3.4. South Korea Market Estimate and Forecast

8.3.5. Singapore Market Estimate and Forecast

8.3.6. Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By Vehicle Type

9.2. By Component

9.3. By Country

9.3.1. Brazil Market Estimate and Forecast

9.3.2. Saudi Arabia Market Estimate and Forecast

9.3.3. South Africa Market Estimate and Forecast

9.3.4. Other Countries Market Estimate and Forecast

10. Company Profiles

10.1. esla

10.1.1. Snapshot

10.1.2. Overview

10.1.3. Offerings

10.1.4. Financial Insight

10.1.5. Recent Developments

10.2. Panasonic

10.2.1. Snapshot

10.2.2. Overview

10.2.3. Offerings

10.2.4. Financial Insight

10.2.5. Recent Developments

10.3. LG Chem

10.3.1. Snapshot

10.3.2. Overview

10.3.3. Offerings

10.3.4. Financial Insight

10.3.5. Recent Developments

10.4. BYD

10.4.1. Snapshot

10.4.2. Overview

10.4.3. Offerings

10.4.4. Financial Insight

10.4.5. Recent Developments

10.5. CATL

10.5.1. Snapshot

10.5.2. Overview

10.5.3. Offerings

10.5.4. Financial Insight

10.5.5. Recent Developments

10.6. Bosch

10.6.1. Snapshot

10.6.2. Overview

10.6.3. Offerings

10.6.4. Financial Insight

10.6.5. Recent Developments

10.7. Siemens

10.7.1. Snapshot

10.7.2. Overview

10.7.3. Offerings

10.7.4. Financial Insight

10.7.5. Recent Developments

10.8. ABB

10.8.1. Snapshot

10.8.2. Overview

10.8.3. Offerings

10.8.4. Financial Insight

10.8.5. Recent Developments

10.9. Continental AG

10.9.1. Snapshot

10.9.2. Overview

10.9.3. Offerings

10.9.4. Financial Insight

10.9.5. Recent Developments

10.10. ZF Friedrichshafen AG

10.10.1. Snapshot

10.10.2. Overview

10.10.3. Offerings

10.10.4. Financial Insight

10.10.5. Recent Developments

10.11. Magna International

10.11.1. Snapshot

10.11.2. Overview

10.11.3. Offerings

10.11.4. Financial Insight

10.11.5. Recent Developments

10.12 Hitachi Automotive Systems

10.12.1. Snapshot

10.12.2. Overview

10.12.3. Offerings

10.12.4. Financial Insight

10.12.5. Recent Developments

10.13. BorgWarner

10.13.1. Snapshot

10.13.2. Overview

10.13.3. Offerings

10.13.4. Financial Insight

10.13.5. Recent Developments

10.14 Denso Corporation

10.14.1. Snapshot

10.14.2. Overview

10.14.3. Offerings

10.14.4. Financial Insight

10.14.5. Recent Developments

10.15. Valeo

10.15.1. Snapshot

10.15.2. Overview

10.15.3. Offerings

10.15.4. Financial Insight

10.15.5. Recent Developments

10.16. Delphi Automotive

10.16.1. Snapshot

10.16.2. Overview

10.16.3. Offerings

10.16.4. Financial Insight

10.16.5. Recent Developments

10.17. GKN Automotive

10.17.1. Snapshot

10.17.2. Overview

10.17.3. Offerings

10.17.4. Financial Insight

10.17.5. Recent Developments

10.18. Toshiba

10.18.1. Snapshot

10.18.2. Overview

10.18.3. Offerings

10.18.4. Financial Insight

10.18.5. Recent Developments

10.19. Robert Bosch GmbH

10.19.1. Snapshot

10.19.2. Overview

10.19.3. Offerings

10.19.4. Financial Insight

10.19.5. Recent Developments

10.20. Johnson Electric

10.20.1. Snapshot

10.20. Overview

10.20.3. Offerings

10.20.4. Financial Insight

10.20.5. Recent Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to availability of information in secondary domain.

List of Tables

Table 1 Applications

Table 2 Study Periods

Table 3 Data Reporting Unit

Table 4 Global Emerging Infectious Disease Diagnostics Market Size, by Technology, 2018-2023 (USD Billion)

Table 5 Global Emerging Infectious Disease Diagnostics Market Size, by Technology, 2025-2030 (USD Billion)

Table 6 Global Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2018-2023 (USD Billion)

Table 7 Global Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2025-2030 (USD Billion)

Table 8 Global Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2018-2023 (USD Billion)

Table 9 Global Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2025-2030 (USD Billion)

Table 8 Global Emerging Infectious Disease Diagnostics Market Size, by Application, 2018-2023 (USD Billion)

Table 9 Global Emerging Infectious Disease Diagnostics Market Size, by Application, 2025-2030 (USD Billion)

Table 8 Global Emerging Infectious Disease Diagnostics Market Size, by End-User, 2018-2023 (USD Billion)

Table 9 Global Emerging Infectious Disease Diagnostics Market Size, by End-User, 2025-2030 (USD Billion)

Table 10 Global Emerging Infectious Disease Diagnostics Market Size, by Region, 2018-2023 (USD Billion)

Table 11 Global Emerging Infectious Disease Diagnostics Market Size, by Region, 2025-2030 (USD Billion)

Table 12 North America Emerging Infectious Disease Diagnostics Market Size, by Technology, 2018-2023 (USD Billion)

Table 13 North America Emerging Infectious Disease Diagnostics Market Size, by Technology, 2025-2030 (USD Billion)

Table 14 North America Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2018-2023 (USD Billion)

Table 15 North America Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2025-2030 (USD Billion)

Table 16 North America Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2018-2023 (USD Billion)

Table 17 North America Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2025-2030 (USD Billion)

Table 16 North America Emerging Infectious Disease Diagnostics Market Size, by Application, 2018-2023 (USD Billion)

Table 17 North America Emerging Infectious Disease Diagnostics Market Size, by Application, 2025-2030 (USD Billion)

Table 16 North America Emerging Infectious Disease Diagnostics Market Size, by End-User, 2018-2023 (USD Billion)

Table 17 North America Emerging Infectious Disease Diagnostics Market Size, by End-User, 2025-2030 (USD Billion)

Table 18 North America Emerging Infectious Disease Diagnostics Market Size, by Country, 2018-2023 (USD Billion)

Table 19 North America Emerging Infectious Disease Diagnostics Market Size, by Country, 2025-2030 (USD Billion)

Table 20 Europe Emerging Infectious Disease Diagnostics Market Size, by Technology, 2018-2023 (USD Billion)

Table 21 Europe Emerging Infectious Disease Diagnostics Market Size, by Technology, 2025-2030 (USD Billion)

Table 22 Europe Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2018-2023 (USD Billion)

Table 23 Europe Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2025-2030 (USD Billion)

Table 24 Europe Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2018-2023 (USD Billion)

Table 25 Europe Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2025-2030 (USD Billion)

Table 26 Europe Emerging Infectious Disease Diagnostics Market Size, by Application, 2018-2023 (USD Billion)

Table 27 Europe Emerging Infectious Disease Diagnostics Market Size, by Application, 2025-2030 (USD Billion)

Table 28 Europe Emerging Infectious Disease Diagnostics Market Size, by End-User, 2018-2023 (USD Billion)

Table 29 Europe Emerging Infectious Disease Diagnostics Market Size, by End-User, 2025-2030 (USD Billion)

Table 30 Europe Emerging Infectious Disease Diagnostics Market Size, by Country, 2018-2023 (USD Billion)

Table 31 Europe Emerging Infectious Disease Diagnostics Market Size, by Country, 2025-2030 (USD Billion)

Table 32 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Technology, 2018-2023 (USD Billion)

Table 33 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Technology, 2025-2030 (USD Billion)

Table 34 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2018-2023 (USD Billion)

Table 35 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2025-2030 (USD Billion)

Table 36 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2018-2023 (USD Billion)

Table 37 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2025-2030 (USD Billion)

Table 38 Europe Emerging Infectious Disease Diagnostics Market Size, by Application, 2018-2023 (USD Billion)

Table 39 Europe Emerging Infectious Disease Diagnostics Market Size, by Application, 2025-2030 (USD Billion)

Table 40 Europe Emerging Infectious Disease Diagnostics Market Size, by End-User, 2018-2023 (USD Billion)

Table 41 Europe Emerging Infectious Disease Diagnostics Market Size, by End-User, 2025-2030 (USD Billion)

Table 42 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Country, 2018-2023 (USD Billion)

Table 43 Asia-Pacific Emerging Infectious Disease Diagnostics Market Size, by Country, 2025-2030 (USD Billion)

Table 44 RoW Emerging Infectious Disease Diagnostics Market Size, by Technology, 2018-2023 (USD Billion)

Table 45 RoW Emerging Infectious Disease Diagnostics Market Size, by Technology, 2025-2030 (USD Billion)

Table 46 RoW Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2018-2023 (USD Billion)

Table 47 RoW Emerging Infectious Disease Diagnostics Market Size, by Disease Type, 2025-2030 (USD Billion)

Table 48 RoW Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2018-2023 (USD Billion)

Table 49 RoW Emerging Infectious Disease Diagnostics Market Size, by Type of Infection, 2025-2030 (USD Billion)

Table 50 RoW Emerging Infectious Disease Diagnostics Market Size, by Application, 2018-2023 (USD Billion)

Table 51 RoW Emerging Infectious Disease Diagnostics Market Size, by Application, 2025-2030 (USD Billion)

Table 52 Europe Emerging Infectious Disease Diagnostics Market Size, by End-User, 2018-2023 (USD Billion)

Table 53 Europe Emerging Infectious Disease Diagnostics Market Size, by End-User, 2025-2030 (USD Billion)

Table 54 RoW Emerging Infectious Disease Diagnostics Market Size, by Country, 2018-2023 (USD Billion)

Table 55 RoW Emerging Infectious Disease Diagnostics Market Size, by Country, 2025-2030 (USD Billion)

Table 56 Snapshot – Abbott Laboratories

Table 57 Snapshot – Becton

Table 58 Snapshot – Dickinson and Company

Table 59 Snapshot – bioMérieux S.A.

Table 60 Snapshot – Bio-Rad Laboratories

Table 61 Snapshot – Co-Diagnostics

Table 62 Snapshot – DANAHER CORPORATION

Table 63 Snapshot – DiaSorin S.p.A.

Table 64 Snapshot – F. Hoffmann-La Roche Ltd

Table 65 Snapshot – Hologic

Table 66 Snapshot – QIAGEN N.V.

Table 67 Snapshot – QuidelOrtho Corporation

Table 68 Snapshot – T2 Biosystems

Table 69 Snapshot – Tecan Trading AG

Table 70 Snapshot – Thermo Fisher Scientific Inc.

Table 71 Snapshot – Siemens Healthineers AG.

List of Figures

Figure 1 Market Coverage

Figure 2 Research Phases

Figure 3 Secondary Technologys for Different Parameters

Figure 4 Methodology

Figure 5 Data Mining & Exploration

Figure 6 Data Triangulation

Figure 7 Assumptions for Market Estimation and Forecast

Figure 8 Market Synopsis

Figure 9 Global Emerging Infectious Disease Diagnostics - Growth Drivers and Restraints

Figure 10 Competitive Benchmark

Figure 11 Global Emerging Infectious Disease Diagnostics Highlight

Figure 12 Global Emerging Infectious Disease Diagnostics Size, by Technology, 2018 - 2030 (USD Billion)

Figure 13 Global Emerging Infectious Disease Diagnostics Size, by Disease Type 2018 - 2030 (USD Billion)

Figure 14 Global Emerging Infectious Disease Diagnostics Size, by Type of Infection 2018 - 2030 (USD Billion)

Figure 15 Global Emerging Infectious Disease Diagnostics Size, by Application 2018 - 2030 (USD Billion)

Figure 15 Global Emerging Infectious Disease Diagnostics Size, by End-User 2018 - 2030 (USD Billion)

Figure 16 Global Emerging Infectious Disease Diagnostics Size, by Region, 2018 - 2030 (USD Billion)

Figure 17 North America Emerging Infectious Disease Diagnostics Highlight

Figure 18 North America Emerging Infectious Disease Diagnostics Size, by Technology, 2018 - 2030 (USD Billion)

Figure 19 North America Emerging Infectious Disease Diagnostics Size, by Disease Type 2018 - 2030 (USD Billion)

Figure 20 North America Emerging Infectious Disease Diagnostics Size, by Type of Infection 2018 - 2030 (USD Billion)

Figure 21 North America Emerging Infectious Disease Diagnostics Size, by Application 2018 - 2030 (USD Billion)

Figure 21 North America Emerging Infectious Disease Diagnostics Size, by End-User 2018 - 2030 (USD Billion)

Figure 22 North America Emerging Infectious Disease Diagnostics Size, by Country, 2018 - 2030 (USD Billion)

Figure 23 Europe Emerging Infectious Disease Diagnostics Highlight

Figure 24 Europe Emerging Infectious Disease Diagnostics Size, by Technology, 2018 - 2030 (USD Billion)

Figure 25 Europe Emerging Infectious Disease Diagnostics Size, by Disease Type 2018 - 2030 (USD Billion)

Figure 26 Europe Emerging Infectious Disease Diagnostics Size, by Type of Infection 2018 - 2030 (USD Billion)

Figure 27 Europe Emerging Infectious Disease Diagnostics Size, by Application 2018 - 2030 (USD Billion)

Figure 27 Europe Emerging Infectious Disease Diagnostics Size, by End-User 2018 - 2030 (USD Billion)

Figure 28 Europe Emerging Infectious Disease Diagnostics Size, by Country, 2018 - 2030 (USD Billion)

Figure 29 Asia-Pacific Emerging Infectious Disease Diagnostics Highlight

Figure 30 Asia-Pacific Emerging Infectious Disease Diagnostics Size, by Technology, 2018 - 2030 (USD Billion)

Figure 31 Asia-Pacific Emerging Infectious Disease Diagnostics Size, by Disease Type 2018 - 2030 (USD Billion)

Figure 32 Asia-Pacific Emerging Infectious Disease Diagnostics Size, by Type of Infection 2018 - 2030 (USD Billion)

Figure 33 Asia-Pacific Emerging Infectious Disease Diagnostics Size, by Application 2018 - 2030 (USD Billion)

Figure 34 RoW Emerging Infectious Disease Diagnostics Size, by End-User 2018 - 2030 (USD Billion)

Figure 35 Asia-Pacific Emerging Infectious Disease Diagnostics Size, by Country, 2018 - 2030 (USD Billion)

Figure 36 RoW Emerging Infectious Disease Diagnostics Highlight

Figure 37 RoW Emerging Infectious Disease Diagnostics Size, by Technology, 2018 - 2030 (USD Billion)

Figure 38 RoW Emerging Infectious Disease Diagnostics Size, by Disease Type 2018 - 2030 (USD Billion)

Figure 39 RoW Emerging Infectious Disease Diagnostics Size, by Type of Infection 2018 - 2030 (USD Billion)

Figure 40 RoW Emerging Infectious Disease Diagnostics Size, by Application 2018 - 2030 (USD Billion)

Figure 41 RoW Emerging Infectious Disease Diagnostics Size, by End-User 2018 - 2030 (USD Billion)

Figure 42 RoW Emerging Infectious Disease Diagnostics Size, by Country, 2018 - 2030 (USD Billion)

Global Emerging Infectious Disease Diagnostics Market Report offers a comprehensive market segmentation analysis along with an estimation for the forecast period 2025-2030

Segments covered in the report

Technology Insight and Forecast 2025-2030

- Polymerase Chain Reaction (PCR)

- Isothermal Nucleic Acid Amplification Technology (INAAT)

- Next-Generation Sequencing (NGS)

- Immunodiagnostics

Type of Infection Insight and Forecast 2025-2030

- Bacterial

- Viral

- Fungal

- Other Infections

Disease Type Insight and Forecast 2025-2030

- Respiratory Infections

- Sexually Transmitted Infections (STIs)Above 50%

- Gastrointestinal Infections

Application Insight and Forecast 2025-2030

- Laboratory Testing and Point-of-Care Testing

End-User Insight and Forecast 2025-2030

- Hospitals and Clinics

- Diagnostics Laboratories

Global Emerging Infectious Disease Diagnostics Market by Region

North America

- By Technology

- By Disease Type

- By Type of Infection

- By Application

- By End-User

- By Country – U.S., Canada, and Mexico

Europe

- By Technology

- By Disease Type

- By Type of Infection

- By Application

- By End-User

- By Country – Germany, U.K., France, Italy, Spain, Russia, and Rest of Europe

Asia-Pacific (APAC)

- By Technology

- By Disease Type

- By Type of Infection

- By Application

- By End-User

- By Country – China, Japan, India, South Korea, and Rest of Asia-Pacific

Rest of the World (RoW)

- By Technology

- By Disease Type

- By Type of Infection

- By Application

- By End-User

- By Country – Brazil, Saudi Arabia, South Africa, U.A.E., and Other Countries

Vynz Research know in your business needs, you required specific answers pertaining to the market, Hence, our experts and analyst can provide you the customized research support on your specific needs.

After the purchase of current report, you can claim certain degree of free customization within the scope of the research.

Please let us know, how we can serve you better with your specific requirements to your research needs. Vynz research promises for quick reversal for your current business requirements.

- Abbott Laboratories

- Becton

- Dickinson and Company

- BioMérieux S.A.

- Bio-Rad Laboratories Inc.

- Co-Diagnostics Inc.

- DANAHER CORPORATION

- DiaSorin S.p.A.

- F. Hoffmann-La Roche Ltd

- Hologic Inc.

- QIAGEN N.V.

- QuidelOrtho Corporation

- T2 Biosystems Inc.

- Tecan Trading AG

- Thermo Fisher Scientific Inc

- Siemens Healthineers AG

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverabvle

Connect With Our Sales Team

- Toll-Free: 1 888 253 3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Emerging Infectious Disease Diagnostics Market