- 1-888-253-3960

- enquiry@vynzresearch.com

-

This is lorem ipsum doller

Hematologic Malignancies Testing Market

| Status : Published | Published On : Sep, 2024 | Report Code : VRHC1289 | Industry : Healthcare | Available Format :

|

Page : 198 |

Global Hematologic Malignancies Testing Market Size & Share | Growth Forecast Report 2030

Industry Insights By Test Types (Complete Blood Count (CBC), Flow Cytometry, Molecular Testing, Genetic Testing and Others), By Technology (Polymerase Chain Reaction (PCR), Next-Generation Sequencing (NGS), Immunohisto Chemistry (IHC), Cytogenetics and Others), By Application (Leukemia, Lymphoma, Myeloma and Others), By Therapy (Chemotherapy, Immunotherapy, Targeted Therapy and Other Therapies), By End User (Hospitals, Diagnostic Labs, Academic and Research Institutions and Others) and By Geography (North America, Europe and Asia Pacific)

Industry Overview

The global Hematologic Malignancies Testing market was estimated at USD 3.3 billion in 2023 and is expected to grow up to USD 13.6 billion by 2030, registering a CAGR of 14.7% during the forecast period ranging between 2025 and 2030.

Global Hematologic Malignancies Testing Market: Industry Overview

Hematologic malignancies refer to specific types of blood cancers such as leukemia, myeloma, and lymphoma. These diseases need effective detection and proper monitoring of the treatment, and these need advanced diagnostic techniques, such ashematologic malignancies testing. These tests help in determining the presence and type of blood cancers. The healthcare professionals can then create tailor treatment plans based on the severity of the disease. The demand for such testing is expected to grow during the forecast period due to the rising prevalence of cancer on a global scale. This will fuel the growth of the market during the projected period, coupled with the rising awareness among patients regarding early diagnosis. Furthermore, advanced technologies, including flow cytometry, molecular diagnostics, and next-generation sequencing (NGS) offer more precise and faster results, which drives the market forward.

Global Hematologic Malignancies Testing Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2018 - 2023 |

|

Base Year Considered |

2024 |

|

Forecast Period |

2025 - 2030 |

|

Market Size in 2024 |

U.S.D. 3.3 Billion |

|

Revenue Forecast in 2030 |

U.S.D. 13.6 Billion |

|

Growth Rate |

14.7% |

|

Segments Covered in the Report |

By Test Types, By Technology, By Application, By Theraphy, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Impact of COVID-19; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe and Asia Pacific |

Despite the significant growth potential, the market faces significant challenges, such as the strict regulatory frameworks and high cost of advanced tests, this restricts widespread adoption and growth of the market. Nevertheless, significant growth in the research activities and healthcare investments along with the growing government initiativesin developing economies offer significant opportunities for market growth.

Global Hematologic Malignancies Testing Industry Dynamics

Global Hematologic Malignancies Testing Market Trends / Growth Drivers:

Increasing shift towards personalized medicine

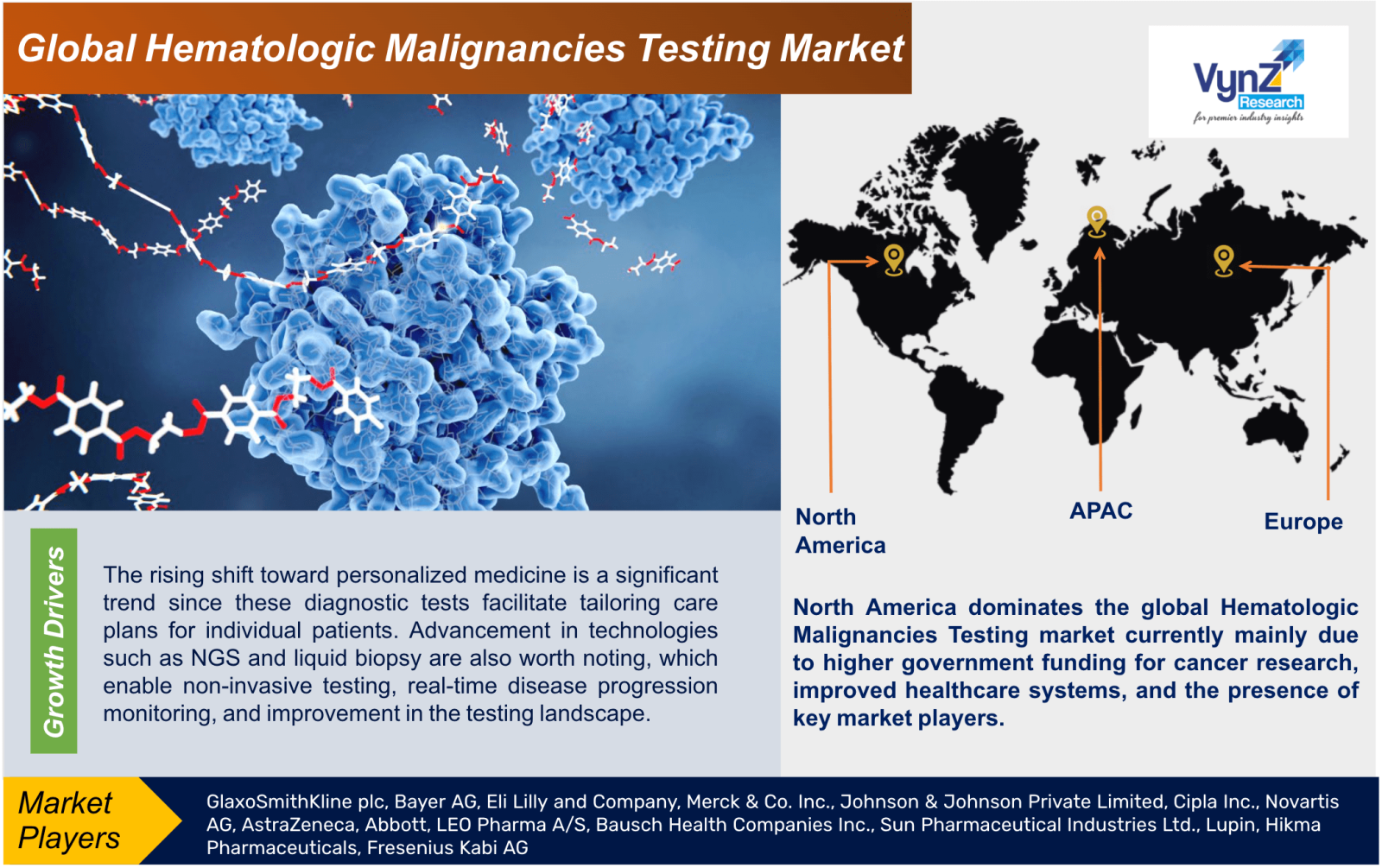

There are several trends witnessed in the global Hematologic Malignancies Testing market and is shaping its future. For example, the rising shift toward personalized medicine is a significant trend since these diagnostic tests facilitate tailoring care plans for individual patients. Advancement in technologies such as NGS and liquid biopsy are also worth noting, which enable non-invasive testing, real-time disease progression monitoring, and improvement in the testing landscape. Furthermore, the industry is also witnessing a growing initiative of collaboration among the pharmaceutical firms and diagnostic companies for improving diagnostics.

One of the significant growth drivers of the global Hematologic Malignancies Testing market is the rising prevalence of leukemia, lymphoma, and other hematologic malignancies. This significant rise in such diseases pushes the demand for advanced, accurate, and faster diagnostic testing, thereby pushing the market forward. Furthermore, the notable swing toward personalized medicine has also driven the demand for precise testing tools like NGS and molecular diagnostics to identify genetic mutations and design targeted treatment plans. The significant rise in government funding for cancer research and healthcare modifications to improve early detection is also contributing to the market expansion.

Global Hematologic Malignancies Testing Market Challenges:

Stringent regulations and high cost of advanced diagnostic tools

While the market has a significant growth potential, there are a few specific challenges that hinder its expansion. For example, the high cost of advanced diagnostic tools such as molecular testing and NGS limits its adoption and widespread use particular in low- and middle-income economies. Furthermore, the stringent regulatory frameworks add to the complexity and delays the approval processes. This prevents new technologies from entering the market and, therefore, restricts its expansion. Additionally, lack of professional personnel to conduct such complex tests, healthcare infrastructure limitations, inconsistent reimbursement policies further impede market growth.

Global Extra High Voltage (EHV) Cables Market Opportunities

Improved healthcare infrastructure and higher investments

Nonetheless, developing markets present significant growth prospects to the global Hematologic Malignancies Testing market, predominantly in Asia-Pacific and Latin American regions. This is mainly due to the rapidly improving healthcare infrastructure and higher investments. It is also attributed to technological innovations, AI-driven diagnostics, higher accessibility and cost-effectiveness, higher prevalence of cancer, and strategic partnerships with governments and research institutions to create better testing solutions.

Global Hematologic Malignancies Testing Market Segmentation

VynZ Research provides an analysis of the key trends in each segment of the global Hematologic Malignancies Testing Market report, along with forecasts at the global, regional and country levels from 2025-2030. Our report has categorized the market based on test types, technology, application, theraphy, end user.

Insight by Test Type

- Complete Blood Count (CBC)

- Flow Cytometry

- Molecular Testing

- Genetic Testing

- Others

Molecular testing segment accounts for the largest share in the market

The global Hematologic Malignancies Testing market is segmented by test type into complete blood count (CBC), flow cytometry, molecular testing, genetic testing, and others. Among all these segments, the molecular testing category holds the largest market share and is expected to dominate the market during the forecast period due to its high accuracy and efficiency in detecting genetic mutations related to blood cancers. Furthermore, within this particular segment, the Next-Generation Sequencing (NGS) is more likely to drive growth due to its ability to provide more comprehensive and faster results. The flow cytometry segment is also projected to grow due to its higher adoption in clinical laboratories and efficiency in diagnosing leukemia and lymphoma.

Insight by Technology

- Polymerase Chain Reaction (PCR)

- Next-Generation Sequencing (NGS)

- Immunohisto Chemistry (IHC)

- Cytogenetics

- Others

Polymerase chain reaction (PCR) segment accounts for the largest share in the market

Based on technology, the global Hematologic Malignancies Testing market is divided into polymerase chain reaction (PCR), Next-Generation Sequencing (NGS), immunohisto chemistry (IHC), cytogenetics, and others. However, out of all these segmentations, it is the PCR technology segment that currently holds the larger market share and is expected to grow at a higher CAGR during the forecast period due to its widespread adoption and use in detecting genetic mutations and minimal residual diseases. However, the NGS technology is increasingly gaining popularity due to its ability to support in-depth genomic data which leads to more targeted treatments.

Insight by Application

- Leukemia

- Lymphoma

- Myeloma

- Others

Polymerase chain reaction (PCR) category reports for the largest share in the market

The global Hematologic Malignancies Testing market is also divided by application into leukemia, lymphoma, myeloma, and others. In comparison to all other segments, the leukemia segment dominates the market. This is mainly attributed to its high incidence rate among all hematologic cancers. On the other hand, testing for lymphoma is also likely to witness substantial growth during the forecast period, especially non-Hodgkin lymphoma, due to the developments in diagnostic technologies and growing research activities on this particular type of cancer.

Insight by Theraphy

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Other

Chemotherapy section reported for the largest share in the market

Different types of therapies also divide the global Hematologic Malignancies Testing market into different sections, such as chemotherapy, immunotherapy, targeted therapy, and other therapies. Out of all these segments, it is the chemotherapy section that dominates the market with its largest revenue share and is expected to lead during the analysis period. This growth is primarily driven by the improved healthcare infrastructure leading to better accessibility, growing number of cancer diagnoses, the development of new cancer treatments. Furthermore, the continual research and clinical trials continue to extend its application possibilities. However, the immunotherapy section is also expected to grow at a significant rate during the same period due to rising number of cancer diagnoses, improved healthcare infrastructure, higher adoption of targeted therapies, and the approval of novel therapies.

Insight by End User

- Hospitals

- Diagnostic Labs

- Academic and Research Institutions

- Others

Diagnostic Laboratories segment accounts for the largest share in the market

Different end users also segregate the global Hematologic Malignancies Testing market into hospitals, diagnostic labs, academic and research institutions and others. Out of them, the diagnostic laboratories section holds the largest share of the market due to the use of sophisticated equipment and rising demand for specialized testing services. The hospitals section, however, is also expected to see significant growth during the projected period due to higher investments by the institutions in-house diagnostic capabilities to offer better patient care and reduce turnaround times.

Global Hematologic Malignancies Testing Market: Geographic Overview

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific (APAC)

- China

- Japan

- India

- South Korea

- Vietnam

- Thailand

- Malaysia

- Rest of Asia-Pacific

- Rest of the World (RoW)

- Brazil

- Saudi Arabia

- South Africa

- U.A.E.

- Other Countries

North America dominates the global Hematologic Malignancies Testing market currently mainly due to higher government funding for cancer research, improved healthcare systems, and the presence of key market players.

The European market is however expected to grow at a steady rate during the forecast period due to the growing incidence of blood cancers, higher demand for advanced and early diagnostics, and higher contributions by countries like Germany, France, and the UK due to their robust healthcare infrastructure and rising investments in cancer research.

The Asia-Pacific region of the market is likely to experience growth at the highest CAGR during the projected period due to the growing prevalence of hematologic cancers, higher healthcare investments, improved diagnostic infrastructure in developing countries like India, China, and Japan, as well as the growing awareness of early detection of cancer and expanding patient population.

Global Hematologic Malignancies Testing Market Competitive Insight

The report provides a comprehensive analysis of the competitive landscape in the market. Some of the key players in the market include:

- GlaxoSmithKline plc

- Bayer AG

- Eli Lilly and Company

- Merck & Co. Inc.

- Johnson & Johnson Private Limited

- Cipla Inc.

- Novartis AG

- AstraZeneca

- Abbott

- LEO Pharma A/S

- Bausch Health Companies Inc.

- Sun Pharmaceutical Industries Ltd.

- Lupin

- Hikma Pharmaceuticals

- Fresenius Kabi AG

Recent Developments by Key Players

Eli Lilly and Company has expanded USD 1 billion of its Limerick, Ireland, manufacturing site to increase production of biologic active ingredients along with its recently approved treatment for early symptomatic Alzheimer's disease.

Abbott Label has started its new RFID converting plant in Nashville. This new facility provides cutting-edge RFID solutions and has expand its capabilities to meet evolving needs like high-speed RFID printing and encoding systems, quality control & testing equipment and precision diecutting & converting machinery.

.png "Hematologic Malignancies Testing Market Size and Market Analysis")

Source: VynZ Research

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By Test Types

1.2.2. By Technology

1.2.3. By Application

1.2.4. By Therapy

1.2.5. By End User

1.2.6. By Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1. Primary Research

1.5.1.2. Secondary Research

1.5.2. Methodology

1.5.2.1. Data Exploration

1.5.2.2. Forecast Parameters

1.5.2.3. Data Validation

1.5.2.4. Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2030

5. Market Segmentation Estimate and Forecast

5.1. By Test Types

5.1.1. Complete Blood Count (CBC)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2030

5.1.2. Flow Cytometry

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2030

5.1.3. Molecular Testing, Genetic Testing

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2030

5.2. By Technology

5.2.1. Polymerase Chain Reaction (PCR)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2030

5.2.2. Next-Generation Sequencing (NGS)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2030

5.2.3. Immunohistology Chemistry (IHC)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2030

5.2.4. Cytogenetics

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2030

5.3 By Application

5.3.1. Leukemia

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2030

5.3.2. Lymphoma

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2030

5.3.3. Myeloma

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2030

5.4. By Therapy

5.4.1. Chemotherapy

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2030

5.4.2. Immunotherapy

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2030

5.4.3. Targeted Therapy

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2030

5.5. By End User

5.5.1. Hospitals

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2030

5.5.2. Diagnostic Labs

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2030

5.5.3. Academic and Research Institutions

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2030

6. North America Market Estimate and Forecast

6.1. By Test Types

6.2. By Technology

6.3. By Application

6.4. By Therapy

6.5. By End User

6.6.1. U.S. Market Estimate and Forecast

6.6.2. Canada Market Estimate and Forecast

6.6.3. Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By Test Types

7.2. By Technology

7.3. By Application

7.4. By Therapy

7.5. By End User

7.6.1. Germany Market Estimate and Forecast

7.6.2. France Market Estimate and Forecast

7.6.3. U.K. Market Estimate and Forecast

7.6.4. Italy Market Estimate and Forecast

7.6.5. Spain Market Estimate and Forecast

7.6.6. Rest of Europe Market Estimate and Forecast

8. Asia-Pacific Market Estimate and Forecast

8.1. By Test Types

8.2. By Technology

8.3. By Application

8.4. By Therapy

8.5 By End User

8.6. By Country – China, Japan, India, South Korea, and Rest of Asia-Pacific

8.6.1. China Market Estimate and Forecast

8.6.2. Japan Market Estimate and Forecast

8.6.3. India Market Estimate and Forecast

8.6.4. South Korea Market Estimate and Forecast

8.6.5. Singapore Market Estimate and Forecast

8.6.6. Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By Test Types

9.2. By Technology

9.3. By Application

9.4. By Therapy

9.5. By End User

9.6. By Country – Brazil, Saudi Arabia, South Africa, U.A.E., and Other Countries

9.6.1. Brazil Market Estimate and Forecast

9.6.2. Saudi Arabia Market Estimate and Forecast

9.6.3. South Africa Market Estimate and Forecast

9.6.4. Other Countries Market Estimate and Forecast

10. Company Profiles

10.1. GlaxoSmithKline plc

10.1.1. Snapshot

10.1.2. Overview

10.1.3. Offerings

10.1.4. Financial Insight

10.1.5. Recent Developments

10.2. Bayer AG

10.2.1. Snapshot

10.2.2. Overview

10.2.3. Offerings

10.2.4. Financial Insight

10.2.5. Recent Developments

10.3. Eli Lilly and Company

10.3.1. Snapshot

10.3.2. Overview

10.3.3. Offerings

10.3.4. Financial Insight

10.3.5. Recent Developments

10.4. Merck & Co. Inc.

10.4.1. Snapshot

10.4.2. Overview

10.4.3. Offerings

10.4.4. Financial Insight

10.4.5. Recent Developments

10.5. Johnson & Johnson Private Limited

10.5.1. Snapshot

10.5.2. Overview

10.5.3. Offerings

10.5.4. Financial Insight

10.5.5. Recent Developments

10.6. Cipla Inc.

10.6.1. Snapshot

10.6.2. Overview

10.6.3. Offerings

10.6.4. Financial Insight

10.6.5. Recent Developments

10.7. Novartis AG

10.7.1. Snapshot

10.7.2. Overview

10.7.3. Offerings

10.7.4. Financial Insight

10.7.5. Recent Developments

10.8. AstraZeneca

10.8.1. Snapshot

10.8.2. Overview

10.8.3. Offerings

10.8.4. Financial Insight

10.8.5. Recent Developments

10.9. Abbott

10.9.1. Snapshot

10.9.2. Overview

10.9.3. Offerings

10.9.4. Financial Insight

10.9.5. Recent Developments

10.10. Abbott

10.10.1. Snapshot

10.10.2. Overview

10.10.3. Offerings

10.10.4. Financial Insight

10.10.5. Recent Developments

10.11. Abbott

10.11.1. Snapshot

10.11.2. Overview

10.11.3. Offerings

10.11.4. Financial Insight

10.11.5. Recent Developments

10.12. Abbott

10.12.1. Snapshot

10.12.2. Overview

10.12.3. Offerings

10.12.4. Financial Insight

10.12.5. Recent Developments

10.13. LEO Pharma A/S

10.13.1. Snapshot

10.13.2. Overview

10.13.3. Offerings

10.13.4. Financial Insight

10.13.5. Recent Developments

10.14. Bausch Health Companies Inc.

10.14.1. Snapshot

10.14.2. Overview

10.14.3. Offerings

10.14.4. Financial Insight

10.14.5. Recent Developments

10.15. Sun Pharmaceutical Industries Ltd.

10.15.1. Snapshot

10.15.2. Overview

10.15.3. Offerings

10.15.4. Financial Insight

10.15.5. Recent Developments

10.16. Lupin

10.16.1. Snapshot

10.16.2. Overview

10.16.3. Offerings

10.16.4. Financial Insight

10.16.5. Recent Developments

10.17. Hikma Pharmaceuticals

10.17.1. Snapshot

10.17.2. Overview

10.17.3. Offerings

10.17.4. Financial Insight

10.17.5. Recent Developments

10.18. Fresenius Kabi AG

10.18.1. Snapshot

10.18.2. Overview

10.18.3. Offerings

10.18.4. Financial Insight

10.18.5. Recent Development

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

List of Tables

Table 1 Test Types

Table 2 Study Periods

Table 3 Data Reporting Unit

Table 4 Global Hematologic Malignancies Testing Market Size, by Test Types, 2018-2023 (USD Billion)

Table 5 Global Hematologic Malignancies Testing Market Size, by Test Types, 2025-2030 (USD Billion)

Table 6 Global Hematologic Malignancies Testing Market Size, by Technology, 2018-2023 (USD Billion)

Table 7 Global Hematologic Malignancies Testing Market Size, by Technology, 2025-2030 (USD Billion)

Table 8 Global Hematologic Malignancies Testing Market Size, by Application , 2018-2023 (USD Billion)

Table 9 Global Hematologic Malignancies Testing Market Size, by Application , 2025-2030 (USD Billion)

Table 10 Global Hematologic Malignancies Testing Market Size, by Therapy, 2018-2023 (USD Billion)

Table 11 Global Hematologic Malignancies Testing Market Size, by Therapy, 2025-2030 (USD Billion)

Table 12 Global Hematologic Malignancies Testing Market Size, by End User, 2018-2023 (USD Billion)

Table 13 Global Hematologic Malignancies Testing Market Size, by End User, 2025-2030 (USD Billion)

Table 14 Global Hematologic Malignancies Testing Market Size, by Region, 2018-2023 (USD Billion)

Table 15 Global Hematologic Malignancies Testing Market Size, by Region, 2025-2030 (USD Billion)

Table 16 North America Hematologic Malignancies Testing Market Size, by Test Types, 2018-2023 (USD Billion)

Table 17 North America Hematologic Malignancies Testing Market Size, by Test Types, 2025-2030 (USD Billion)

Table 18 North America Hematologic Malignancies Testing Market Size, by Technology, 2018-2023 (USD Billion)

Table 19 North America Hematologic Malignancies Testing Market Size, by Technology, 2025-2030 (USD Billion)

Table 20 North America Hematologic Malignancies Testing Market Size, by Application, 2018-2023 (USD Billion)

Table 21 North America Hematologic Malignancies Testing Market Size, by Application, 2025-2030 (USD Billion)

Table 22 North America Hematologic Malignancies Testing Market Size, by Therapy, 2018-2023 (USD Billion)

Table 23 North America Hematologic Malignancies Testing Market Size, by Therapy, 2025-2030 (USD Billion)

Table 24 North America Hematologic Malignancies Testing Market Size, by End User, 2018-2023 (USD Billion)

Table 25 North America Hematologic Malignancies Testing Market Size, by End User, 2025-2030 (USD Billion)

Table 26 North America Hematologic Malignancies Testing Market Size, by Country, 2018-2023 (USD Billion)

Table 27 North America Hematologic Malignancies Testing Market Size, by Country, 2025-2030 (USD Billion)

Table 28 Europe Hematologic Malignancies Testing Market Size, by Test Types, 2018-2023 (USD Billion)

Table 29 Europe Hematologic Malignancies Testing Market Size, by Test Types, 2025-2030 (USD Billion)

Table 30 Europe Hematologic Malignancies Testing Market Size, by Technology, 2018-2023 (USD Billion)

Table 31 Europe Hematologic Malignancies Testing Market Size, by Technology, 2025-2030 (USD Billion)

Table 32 Europe Hematologic Malignancies Testing Market Size, by Application, 2018-2023 (USD Billion)

Table 33 Europe Hematologic Malignancies Testing Market Size, by Application, 2025-2030 (USD Billion)

Table 34 Europe Hematologic Malignancies Testing Market Size, by Therapy, 2018-2023 (USD Billion)

Table 35 Europe Hematologic Malignancies Testing Market Size, by Therapy, 2025-2030 (USD Billion)

Table 36 Europe Hematologic Malignancies Testing Market Size, by End User, 2018-2023 (USD Billion)

Table 37 Europe Hematologic Malignancies Testing Market Size, by End User, 2025-2030 (USD Billion)

Table 38 Europe Hematologic Malignancies Testing Market Size, by Country, 2018-2023 (USD Billion)

Table 39 Europe Hematologic Malignancies Testing Market Size, by Country, 2025-2030 (USD Billion)

Table 40 Asia-Pacific Hematologic Malignancies Testing Market Size, by Test Types, 2018-2023 (USD Billion)

Table 41 Asia-Pacific Hematologic Malignancies Testing Market Size, by Test Types, 2025-2030 (USD Billion)

Table 42 Asia-Pacific Hematologic Malignancies Testing Market Size, by Technology, 2018-2023 (USD Billion)

Table 43 Asia-Pacific Hematologic Malignancies Testing Market Size, by Technology, 2025-2030 (USD Billion)

Table 44 Asia-Pacific Hematologic Malignancies Testing Market Size, by Application, 2018-2023 (USD Billion)

Table 45 Asia-Pacific Hematologic Malignancies Testing Market Size, by Application, 2025-2030 (USD Billion)

Table 46 Europe Hematologic Malignancies Testing Market Size, by Therapy, 2018-2023 (USD Billion)

Table 47 Europe Hematologic Malignancies Testing Market Size, by Therapy, 2025-2030 (USD Billion)

Table 48 Europe Hematologic Malignancies Testing Market Size, by End User, 2018-2023 (USD Billion)

Table 49 Europe Hematologic Malignancies Testing Market Size, by End User, 2025-2030 (USD Billion)

Table 50 Asia-Pacific Hematologic Malignancies Testing Market Size, by Country, 2018-2023 (USD Billion)

Table 51 Asia-Pacific Hematologic Malignancies Testing Market Size, by Country, 2025-2030 (USD Billion)

Table 52 RoW Hematologic Malignancies Testing Market Size, by Test Types, 2018-2023 (USD Billion)

Table 53 RoW Hematologic Malignancies Testing Market Size, by Test Types, 2025-2030 (USD Billion)

Table 54 RoW Hematologic Malignancies Testing Market Size, by Technology, 2018-2023 (USD Billion)

Table 55 RoW Hematologic Malignancies Testing Market Size, by Technology, 2025-2030 (USD Billion)

Table 56 RoW Hematologic Malignancies Testing Market Size, by Application, 2018-2023 (USD Billion)

Table 57 RoW Hematologic Malignancies Testing Market Size, by Application, 2025-2030 (USD Billion)

Table 58 RoW Hematologic Malignancies Testing Market Size, by Therapy, 2018-2023 (USD Billion)

Table 59 RoW Hematologic Malignancies Testing Market Size, by Therapy, 2025-2030 (USD Billion)

Table 60 RoW Hematologic Malignancies Testing Market Size, by End User, 2018-2023 (USD Billion)

Table 61 RoW Hematologic Malignancies Testing Market Size, by End User, 2025-2030 (USD Billion)

Table 62 RoW Hematologic Malignancies Testing Market Size, by Country, 2018-2023 (USD Billion)

Table 63 RoW Hematologic Malignancies Testing Market Size, by Country, 2025-2030 (USD Billion)

Table 64 Snapshot – GlaxoSmithKline plc

Table 65 Snapshot – Bayer AG

Table 66 Snapshot – Eli Lilly and Company

Table 67 Snapshot – Merck & Co. Inc.

Table 68 Snapshot – Johnson & Johnson Private Limited

Table 69 Snapshot – Cipla Inc.

Table 70 Snapshot – Novartis AG

Table 71 Snapshot – AstraZeneca

Table 72 Snapshot – Abbott

Table 73 Snapshot – LEO Pharma A/S

Table 74 Snapshot – Bausch Health Companies Inc.

Table 75 Snapshot – Sun Pharmaceutical Industries Ltd.

Table 76 Snapshot – Lupin

Table 77 Snapshot – Hikma Pharmaceuticals

Table 78 Snapshot – Fresenius Kabi AG

List of Figures

Figure 1 Market Application

Figure 2 Research Phases

Figure 3 Secondary Test Types for Different Parameters

Figure 4 Methodology

Figure 5 Data Mining & Exploration

Figure 6 Data Triangulation

Figure 7 Assumptions for Market Estimation and Forecast

Figure 8 Market Synopsis

Figure 9 Global Hematologic Malignancies Testing Market - Growth Drivers and Restraints

Figure 10 Competitive Benchmark

Figure 11 Global Hematologic Malignancies Testing Market Highlight

Figure 12 Global Hematologic Malignancies Testing Market Size, by Test Types, 2018 – 2030 (USD Billion)

Figure 13 Global Hematologic Malignancies Testing Market Size, by Technology 2018 – 2030 (USD Billion)

Figure 14 Global Hematologic Malignancies Testing Market Size, by Application 2018 – 2030 (USD Billion)

Figure 15 Global Hematologic Malignancies Testing Market Size, by Therapy 2018 – 2030 (USD Billion)

Figure 16 Global Hematologic Malignancies Testing Market Size, by End User 2018 – 2030 (USD Billion)

Figure 17 Global Hematologic Malignancies Testing Market Size, by Region, 2018 – 2030 (USD Billion)

Figure 18 North America Hematologic Malignancies Testing Market Highlight

Figure 19 North America Hematologic Malignancies Testing Market Size, by Test Types, 2018 – 2030 (USD Billion)

Figure 20 North America Hematologic Malignancies Testing Market Size, by Technology 2018–2030 (USD Billion)

Figure 21 North America Hematologic Malignancies Testing Market Size, by Application 2018–2030 (USD Billion)

Figure 22 North America Hematologic Malignancies Testing Market Size, by Therapy 2018–2030 (USD Billion)

Figure 23 North America Hematologic Malignancies Testing Market Size, by End User 2018–2030 (USD Billion)

Figure 24 North America Hematologic Malignancies Testing Market Size, by Country, 2018 – 2030 (USD Billion)

Figure 25 Europe Hematologic Malignancies Testing Market Highlight

Figure 26 Europe Hematologic Malignancies Testing Market Size, by Test Types, 2018 – 2030 (USD Billion)

Figure 27 Europe Hematologic Malignancies Testing Market Size, by Technology 2018 – 2030 (USD Billion)

Figure 28 Europe Hematologic Malignancies Testing Market Size, by Application 2018 – 2030 (USD Billion)

Figure 29 Europe Hematologic Malignancies Testing Market Size, by Therapy 2018 – 2030 (USD Billion)

Figure 30 Europe Hematologic Malignancies Testing Market Size, by End User 2018 – 2030 (USD Billion)

Figure 31 Europe Hematologic Malignancies Testing Market Size, by Country, 2018 – 2030 (USD Billion)

Figure 32 Asia-Pacific Hematologic Malignancies Testing Market Highlight

Figure 33 Asia-Pacific Hematologic Malignancies Testing Market Size, by Test Types, 2018 – 2030 (USD Billion)

Figure 34 Asia-Pacific Hematologic Malignancies Testing Market Size, by Technology 2018 – 2030 (USD Billion)

Figure 35 Asia-Pacific Hematologic Malignancies Testing Market Size, by Application 2018 – 2030 (USD Billion)

Figure 36 Asia-Pacific Hematologic Malignancies Testing Market Size, by Therapy 2018 – 2030 (USD Billion)

Figure 37 Asia-Pacific Hematologic Malignancies Testing Market Size, by End User 2018 – 2030 (USD Billion)

Figure 38 Asia-Pacific Hematologic Malignancies Testing Market Size, by Country, 2018 – 2030 (USD Billion)

Figure 39 RoW Hematologic Malignancies Testing Market Highlight

Figure 40 RoW Hematologic Malignancies Testing Market Size, by Test Types, 2018 – 2030 (USD Billion)

Figure 41 RoW Hematologic Malignancies Testing Market Size, by Technology 2018 – 2030 (USD Billion)

Figure 42 RoW Hematologic Malignancies Testing Market Size, by Application 2018 – 2030 (USD Billion)

Figure 43 RoW Hematologic Malignancies Testing Market Size, by Therapy 2018 – 2030 (USD Billion)

Figure 44 RoW Hematologic Malignancies Testing Market Size, by End User 2018 – 2030 (USD Billion)

Figure 45 RoW Hematologic Malignancies Testing Market Size, by Country, 2018 – 2030 (USD Billion)

Global Hematologic Malignancies Testing Market Coverage

By Test Type Insight and Forecast 2025-2030

- Complete Blood Count (CBC)

- Flow Cytometry

- Molecular Testing

- Genetic Testing

By Technology Insight and Forecast 2025-2030

- Polymerase Chain Reaction (PCR)

- Next-Generation Sequencing (NGS)

- Immunohistochemistry (IHC)

- Cytogenetics

By Application Insight and Forecast 2025-2030

- Leukemia

- Lymphoma

- Myeloma

By Therapy

- Different Sections

- Such as Chemotherapy

- Immunotherapy

- Targeted Therapy

- Other Therapies

By End User Insight and Forecast 2025-2030

- Hospitals

- Diagnostic Labs

- Academic and Research Institutions

- Others

Global Hematologic Malignancies Testing Market by Region

North America

- By Test Type

- By Technology

- By Application

- By Therapy

- By End User

- By Country – U.S., Canada, and Mexico

Europe

- By Test Type

- By Technology

- By Application

- By Therapy

- By End User

- By Country – Germany, U.K., France, Italy, Spain, Russia, and Rest of Europe

Asia-Pacific (APAC)

- By Test Type

- By Technology

- By Application

- By Therapy

- By End User

- By Country – China, Japan, India, South Korea, and the Rest of Asia-Pacific

Rest of the World (RoW)

- By Test Type

- By Technology

- By Application

- By Therapy

- By End User

- By Country – Brazil, Saudi Arabia, South Africa, U.A.E., and Other Countries

Vynz Research know in your business needs, you required specific answers pertaining to the market, Hence, our experts and analyst can provide you the customized research support on your specific needs.

After the purchase of current report, you can claim certain degree of free customization within the scope of the research.

Please let us know, how we can serve you better with your specific requirements to your research needs. Vynz research promises for quick reversal for your current business requirements.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverabvle

Connect With Our Sales Team

- Toll-Free: 1 888 253 3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Hematologic Malignancies Testing Market

Global Hematologic Malignancies Testing Market Size & Share | Growth Forecast Report 2030

- The global Hematologic Malignancies Testing market was estimated at USD 3.3 billion in 2023 and is expected to grow up to USD 13.6 billion by 2030, registering a CAGR of 14.7% during the forecast period ranging between 2025 and 2030.

- The market is categorized by different test types, technology, application, therapy, end-user and geography

- The primary growth drivers of the market include growing cancer prevalence, rising adoption of personalized medicine, and advancements in diagnostic technologies.

- Strict regulatory measures and high costs are the challenges that hinder market growth, but opportunities are offered by the emerging markets with their increasing healthcare investments.

- North America dominates the market presently, but the Asia-Pacific region is likely to witness a high growth rate due to significant development in the healthcare infrastructure.