- 1-888-253-3960

- enquiry@vynzresearch.com

-

This is lorem ipsum doller

Next-Generation IVD Market

| Status : Published | Published On : Dec, 2023 | Report Code : VRHC1278 | Industry : Healthcare | Available Format :

|

Page : 225 |

Global Next-Generation IVD Market – Analysis and Forecast (2025-2030)

Industry Insight by Type (core laboratory diagnostics, POC testing, and molecular diagnostics), by Product Type (consumables, instruments, and software), by Application (oncology/cancer, infectious diseases, diabetes, cardiology, and other applications), by End-use Industry (hospitals and clinics, diagnostic laboratories, academic and research institutions, and other end-use industries), and Geography (U.S., Canada, Germany, U.K., France, China, Japan, India, and Rest of the World)

Industry Overview

Next-Generation In Vitro Diagnostics (IVD) refers to advanced technologies and methodologies that revolutionize diagnostic testing outside the human body. It encompasses cutting-edge approaches like molecular diagnostics, genomics, proteomics, and digital pathology, enabling more precise and personalized healthcare. Next-Generation IVD enhances disease detection, monitoring, and treatment by providing rapid, accurate, and comprehensive insights into an individual's health. These innovations empower healthcare professionals to tailor interventions, predict disease risks, and optimize therapeutic strategies, marking a significant leap forward in the field of diagnostics for improved patient outcomes and healthcare efficiency.

Global next-generation IVD market was worth USD 87.40 billion in 2023 and is expected reach USD 125.00 billion by 2030 with a CAGR of 5.11% during the forecast period, i.e., 2025-2030. The growing demand for next-generation IVD is driven by the advancements in genomics and molecular diagnostics, increasing demand for personalized medicine, a focus on early disease detection, and the rise of digital health technologies for more precise and efficient diagnostic capabilities.

Geographically, the global next-generation IVD market is expanding rapidly in North America, Europe, and the Asia Pacific, as a result of the robust healthcare infrastructure, increasing adoption of advanced diagnostic technologies, rising awareness of personalized medicine, and supportive regulatory frameworks; however, the market confronts constraints such as regulatory complexities, reimbursement issues, and the need for standardization. Overall, the next-generation IVD market offers potential prospects for market participants to develop and fulfill the growing needs of wide range of applications including hospitals and clinics, diagnostic laboratories, academic and research institutions.

Next-Generation IVD Market Segmentation

Insight by Type

Based on type, the global next-generation IVD market is segmented into core laboratory diagnostics, POC testing, and molecular diagnostics. Core laboratory diagnostics dominated the next-generation IVD market in 2023 owing to their essential role in routine clinical testing. These labs offer comprehensive services, integrating advanced technologies for precise and high-throughput analysis. For instance, as of my last knowledge update in January 2023, Roche's cobas 6800/8800 systems, introduced in 2014, exemplify core lab dominance, enabling simultaneous testing of multiple pathogens. Additionally, Siemens Healthineers' Atellica Solution, launched in 2017, integrates various diagnostic disciplines. The scalability, efficiency, and broad testing capabilities of such systems highlight their pivotal role, contributing to the dominance of core laboratory diagnostics in the evolving IVD landscape.

Insight by Product Type

Based on product type, the global next-generation IVD market is segmented into consumables, instruments, and software. Consumable panels dominated the global next-generation IVD market in 2022 as they offer cost-effective and scalable solutions for routine testing. Latest examples include Bio-Rad's ddPCR Multiplex Supermix, launched in 2021, providing precise and multiplexed DNA analysis. Additionally, Illumina's TruSight Oncology 500, introduced in 2020, is a comprehensive panel for cancer profiling. These consumable panels enhance efficiency, reduce turnaround times, and enable targeted analysis. The market dominance of consumable panels is underscored by their adaptability across various diagnostic platforms, facilitating widespread adoption and contributing to the dynamic evolution of the next-generation IVD market.

Insight by Application

Based on application, the global next-generation IVD market is segmented into oncology/cancer, infectious diseases, diabetes, cardiology, and other applications. Oncology/cancer segment dominated the global next-generation IVD market in 2023 due to the increasing demand for precision medicine in cancer treatment. Recent examples include Foundation Medicine's FoundationOne Liquid CDx, approved in 2020, which analyzes circulating tumor DNA for comprehensive genomic profiling. Guardant Health's Guardant360, continually updated, is another example, utilizing liquid biopsy for real-time cancer monitoring. The focus on personalized oncology therapies and the rising incidence of cancer globally drives the prominence of oncology in the next-generation IVD market, reflecting the crucial role these diagnostics play in tailoring treatments and improving patient outcomes.

Insight by End-use Industry

Based on end-use industry, the global next-generation IVD market is segmented into hospitals and clinics, diagnostic laboratories, academic and research institutions, and other end-use industries. Hospitals and clinic dominated the global next-generation IVD market in 2023 as they serve as primary hubs for patient diagnostics and healthcare delivery. The demand for advanced diagnostic capabilities is exemplified by Abbott's Alinity-m molecular diagnostics system, launched in 2020, providing comprehensive infectious disease testing. Additionally, Sysmex Corporation's XN-3100, introduced in 2021, enhances hematology diagnostics in clinical settings. The growing patient influx, coupled with the need for rapid and accurate results, underscores the pivotal role of hospitals and clinics in driving the adoption of next-generation IVD technologies, ensuring effective disease management and improved patient care.

Global Next-Generation IVD Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2018 - 2023 |

|

Base Year Considered |

2024 |

|

Forecast Period |

2025 - 2030 |

|

Market Size in 2024 |

U.S.D. 87.40 Billion |

|

Revenue Forecast in 2030 |

U.S.D. 125 Billion |

|

Growth Rate |

5.11% |

|

Segments Covered in the Report |

By Type, By Product Type, By Application and By End-Use Industry |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Impact of COVID-19; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Middle East, and South America |

Industry Dynamics

Next-Generation IVD Market Growth Drivers

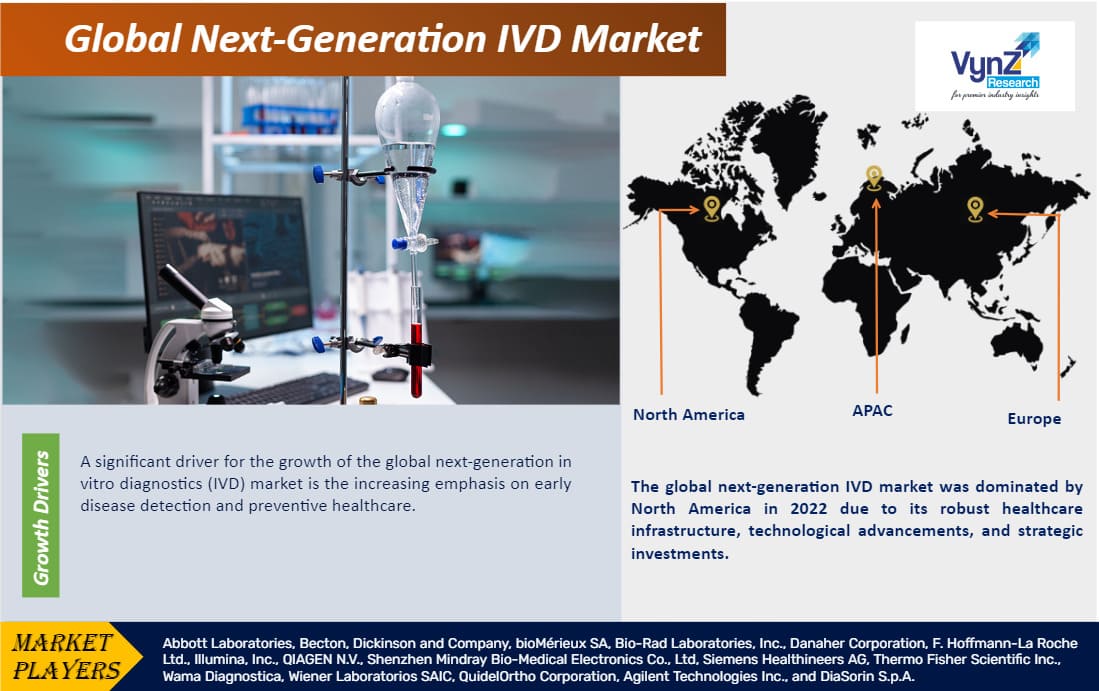

Increasing Emphasis on Early Disease Detection and Preventive Healthcare

A significant driver for the growth of the global next-generation in vitro diagnostics (IVD) market is the increasing emphasis on early disease detection and preventive healthcare. Illumina's introduction of the Grail Galleri test in 2021 exemplifies this trend. Galleri is a multi-cancer early detection blood test designed to identify more than 50 types of cancers at an early, potentially curable stage. This reflects a paradigm shift toward proactive healthcare strategies, aligning with the global push for precision medicine and personalized treatment approaches. The ability of such tests to detect multiple cancer types simultaneously and at early stages enhances the prospects for successful intervention, fostering a broader adoption of Next-Generation IVD in routine clinical practice.

Furthermore, the integration of CRISPR technology in diagnostics, demonstrated by Sherlock Biosciences' Sherlock CRISPR SARS-CoV-2 kit, authorized for Emergency Use in 2020, showcases the market's response to emerging infectious threats. The demand for rapid, accurate, and multiplexed diagnostics, particularly in the context of infectious diseases, propels the growth of Next-Generation IVD, emphasizing its crucial role in global health preparedness and response.

Integration of Artificial Intelligence (AI) and Machine Learning (ML) in Diagnostics

The integration of Artificial Intelligence (AI) and Machine Learning (ML) in diagnostics is a key driver for the growth of the global Next-Generation In Vitro Diagnostics (IVD) market. These technologies enhance the accuracy, efficiency, and personalization of diagnostic processes. For instance, Paige Prostate, introduced in 2021, employs AI for pathology interpretation, aiding in prostate cancer diagnosis. Tempus' Tempus ONE, launched in 2020, utilizes ML to streamline clinical workflows and improve cancer care. These platforms leverage large datasets to identify patterns and correlations that may be imperceptible to human analysis, enabling more precise diagnostics and treatment decisions.

The continual evolution of AI and ML applications in diagnostics is catalyzing innovation, driving the adoption of Next-Generation IVD technologies, and revolutionizing the landscape of medical diagnostics for improved patient outcomes and healthcare efficiency. For instance, PathAI, in collaboration with Bristol Myers Squibb, employs AI-powered pathology solutions to improve diagnostic accuracy and efficiency. This amalgamation of cutting-edge technologies not only enhances diagnostic precision but also underscores the transformative potential of next-generation IVD in reshaping healthcare by enabling more proactive and personalized approaches to disease management.

Next-Generation IVD Market Challenge

End-of-Life Management of Next-Generation IVD

One significant challenge for the next-generation IVD industry is the need for standardization and regulatory harmonization. Differing regulations across regions create complexities in product development, approval processes, and market access. Achieving global standardization is critical for ensuring the seamless integration of advanced diagnostic technologies, fostering innovation, and addressing regulatory uncertainties. Overcoming these challenges is essential to facilitate the widespread adoption of next-generation IVD solutions and unlock their full potential in enhancing healthcare outcomes on a global scale.

Next-Generation IVD Market Geographic Overview

-

North America

-

Europe

-

Asia Pacific (APAC)

-

Middle East and Africa (MEA)

-

South America

The global next-generation IVD market is segmented into North America, Europe, the Asia-Pacific, South America, and the Middle East and Africa region. The global next-generation IVD market was dominated by North America in 2023 due to its robust healthcare infrastructure, technological advancements, and strategic investments. The region is at the forefront of adopting innovative diagnostic solutions. For instance, Exact Sciences' Cologuard, FDA-approved in 2014, revolutionizes colorectal cancer screening through non-invasive methods. Additionally, Illumina's NovaSeq 6000, launched in 2017, exemplifies cutting-edge genomic sequencing. The region's proactive approach in integrating these technologies into clinical practice, coupled with favorable regulatory frameworks, positions North America as a leader in driving the growth and adoption of next-generation IVD technologies.

Next-Generation IVD Market Competitive Insight

Roche holds a prominent position in the next-generation in vitro diagnostics (IVD) market, continually innovating to advance diagnostic capabilities. Notably, the Cobas 6800/8800 systems, introduced in 2014, exemplify Roche's commitment to high-throughput molecular diagnostics, enabling simultaneous testing for multiple pathogens. The system has been pivotal, especially during the COVID-19 pandemic, showcasing Roche's adaptability to emerging healthcare needs. Roche's leadership extends to personalized medicine with Foundation Medicine, a subsidiary, offering comprehensive genomic profiling services. Through these initiatives, Roche remains a key player driving advancements in the next-generation IVD landscape and contributing significantly to the evolution of diagnostic technologies.

Abbott Laboratories is another major player in the Next-Generation In Vitro Diagnostics (IVD) market, known for its innovative solutions. The approval of the Abbott RealTime SARS-CoV-2 assay in 2020 showcased the company's rapid response to the COVID-19 pandemic, providing reliable diagnostic tools. Abbott's Alinity m molecular diagnostics system, launched in 2020, exemplifies its commitment to high-throughput and comprehensive infectious disease testing. The system offers versatility and efficiency in clinical settings. Abbott's strategic focus on cutting-edge diagnostics positions it as a key contributor to advancements in the Next-Generation IVD market, addressing critical healthcare challenges with innovative solutions.

Recent Development by Key Players

In November 2023, Veracyte and Illumina entered a multi-year agreement to develop decentralized in vitro diagnostic (IVD) tests using Illumina’s NextSeq 550Dx next-generation sequencing instrument. This collaboration, part of Veracyte’s multi-platform IVD approach, is aiming to enhance worldwide accessibility of tests like the Percepta Nasal Swab (for diagnosing lung nodules in smokers) and the Prosigna Breast Cancer Assay. Leveraging quantitative polymerase chain reaction (qPCR) and Illumina's technology, the partnership underscores a commitment to advancing diagnostic capabilities, particularly in noninvasive cancer detection and personalized breast cancer treatment decision-making.

In April 2023, Waters Corporation introduced the Xevo TQ Absolute IVD mass spectrometer, an advanced addition to its MassTrak IVD LC-MS/MS Systems for clinical diagnostics. Boasting up to five times greater sensitivity than comparable instruments, it facilitates the precise quantification of clinical analytes, allowing detection at unprecedented low levels. This innovation supports expanded testing capabilities, including less invasive assays like saliva and dried blood spots, making it especially suitable for hospital and commercial labs aiming for sustainability and growth.

Key Players Covered in the Report

Abbott Laboratories, Becton, Dickinson and Company, bioMérieux SA, Bio-Rad Laboratories, Inc., Danaher Corporation, F. Hoffmann-La Roche Ltd., Illumina, Inc., QIAGEN N.V., Shenzhen Mindray Bio-Medical Electronics Co., Ltd, Siemens Healthineers AG, Thermo Fisher Scientific Inc., Wama Diagnostica, Wiener Laboratorios SAIC, QuidelOrtho Corporation, Agilent Technologies Inc., and DiaSorin S.p.A.

The Next-generation IVD market report offers a comprehensive market segmentation analysis along with an estimation for the forecast period 2025–2030.

Segments Covered in the Report

-

By Type

-

Laboratory Diagnostics

-

POC Testing

-

Molecular Diagnostics

-

By Product Type

-

Consumables

-

Instruments

-

Software

-

By Application

-

Oncology/Cancer

-

Infectious Diseases

-

Diabetes

-

Cardiology

-

Other Applications

-

By End-Use Industry

-

Hospitals and Clinics

-

Diagnostic Laboratories

-

Academic and Research Institutions

-

Other end-use industry

Region Covered in the Report

-

North America

-

U.S.

-

Canada

-

Mexico

-

Europe

-

Germany

-

U.K.

-

France

-

Italy

-

Spain

-

Russia

-

Rest of Europe

-

Asia-Pacific (APAC)

-

China

-

Japan

-

India

-

South Korea

-

Rest of Asia-Pacific

-

Middle East and Africa (MEA)

-

Saudi Arabia

-

U.A.E

-

South Africa

-

Rest of MEA

-

South America

-

Argentina

-

Brazil

-

Chile

-

Rest of South America

Primary Research Interviews Breakdown

%20System%20Market.png "Next-Generation IVD Market")

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By Type

1.2.2. By Product Type

1.2.3. By Application

1.2.4. By End-use Industry

1.2.5. By Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1. Primary Research

1.5.1.2. Secondary Research

1.5.2. Methodology

1.5.2.1. Data Exploration

1.5.2.2. Forecast Parameters

1.5.2.3. Data Validation

1.5.2.4. Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2030

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Core Laboratory Diagnostics

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2030

5.1.2. POC Testing

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2030

5.1.3. Molecular Diagnostics

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2030

5.1.4. Unmanned Aerial Vehicle

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2030

5.2. By Product Type

5.2.1. Consumables

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2030

5.2.2. Instruments

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2030

5.2.3. Software

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2030

5.3 By Application

5.3.1. Oncology/Cancer

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2030

5.3.2. Infectious Diseases

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2030

5.3.3. Diabetes

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2030

5.3.4. By Cardiology

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2030

5.4. By End-Use Industry

5.4.1. Hospitals and Clinics

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2030

5.4.2. Diagnostic Laboratories

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2030

5.4.3. Academic and Research Institutions

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2030

5.4.4. Other End-Use Industries

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2030

6. North America Market Estimate and Forecast

6.1. By Type

6.2. By Product Type

6.3. By Application

6.4. By End-Use Industry

6.5.1. Market Estimate and Forecast

6.5.2. Canada Market Estimate and Forecast

6.5.3. Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By Type

7.2. By Product Type

7.3. By Application

7.4. By End-Use Industry

7.5.1. Germany Market Estimate and Forecast

7.5.2. France Market Estimate and Forecast

7.5.3. U.K. Market Estimate and Forecast

7.5.4. Italy Market Estimate and Forecast

7.5.5. Spain Market Estimate and Forecast

7.5.6. Rest of Europe Market Estimate and Forecast

8. Asia-Pacific Market Estimate and Forecast

8.1. By Type

8.2. By Product Type

8.3. By Application

8.4. By End-Use Industry

8.4. By Country – China, Japan, India, South Korea, and Rest of Asia-Pacific

8.5.1. China Market Estimate and Forecast

8.5.2. Japan Market Estimate and Forecast

8.5.3. India Market Estimate and Forecast

8.5.4. South Korea Market Estimate and Forecast

8.5.5. Singapore Market Estimate and Forecast

8.5.6. Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By Type

9.2. By Product Type

9.3. By Application

9.4. By End-Use Industry

9.5. By Country – Brazil, Saudi Arabia, South Africa, U.A.E., and Other Countries

9.5.1. Brazil Market Estimate and Forecast

9.5.2. Saudi Arabia Market Estimate and Forecast

9.5.3. South Africa Market Estimate and Forecast

9.5.4. Other Countries Market Estimate and Forecast

10. Company Profiles

10.1. Abbott Laboratories

10.1.1. Snapshot

10.1.2. Overview

10.1.3. Offerings

10.1.4. Financial Insight

10.1.5. Recent Developments

10.2. Fulcrum BioEnerg Inc.

10.2.1. Snapshot

10.2.2. Overview

10.2.3. Offerings

10.2.4. Financial Insight

10.2.5. Recent Developments

10.3. BioMérieux SA

10.3.1. Snapshot

10.3.2. Overview

10.3.3. Offerings

10.3.4. Financial Insight

10.3.5. Recent Developments

10.4. Bio-Rad Laboratories

10.4.1. Snapshot

10.4.2. Overview

10.4.3. Offerings

10.4.4. Financial Insight

10.4.5. Recent Developments

10.5. Danaher Corporation

10.5.1. Snapshot

10.5.2. Overview

10.5.3. Offerings

10.5.4. Financial Insight

10.5.5. Recent Developments

10.6. F. Hoffmann-La Roche Ltd.

10.6.1. Snapshot

10.6.2. Overview

10.6.3. Offerings

10.6.4. Financial Insight

10.6.5. Recent Developments

10.7. Illumina

10.7.1. Snapshot

10.7.2. Overview

10.7.3. Offerings

10.7.4. Financial Insight

10.7.5. Recent Developments

10.8. QIAGEN N.V.

10.8.1. Snapshot

10.8.2. Overview

10.8.3. Offerings

10.8.4. Financial Insight

10.8.5. Recent Developments

10.9. Shenzhen Mindray Bio-Medical Electronics Co.

10.9.1. Snapshot

10.9.2. Overview

10.9.3. Offerings

10.9.4. Financial Insight

10.9.5. Recent Development

10.10. Siemens Healthineers AG

10.10.1. Snapshot

10.10.2. Overview

10.10.3. Offerings

10.10.4. Financial Insight

10.10.5. Recent Developments

10.11. Thermo Fisher Scientific Inc.

10.11.1. Snapshot

10.11.2. Overview

10.11.3. Offerings

10.11.4. Financial Insight

10.11.5. Recent Developments

10.12. Wama Diagnostica

10.12.1. Snapshot

10.12.2. Overview

10.12.3. Offerings

10.12.4. Financial Insight

10.12.5. Recent Developments

10.13. Wiener Laboratorios SAIC

10.13.1. Snapshot

10.13.2. Overview

10.13.3. Offerings

10.13.4. Financial Insight

10.13.5. Recent Developments

10.14. QuidelOrtho Corporation

10.14.1. Snapshot

10.14.2. Overview

10.14.3. Offerings

10.14.4. Financial Insight

10.14.5. Recent Developments

10.15. Agilent Technologies Inc.

10.15.1. Snapshot

10.15.2. Overview

10.15.3. Offerings

10.15.4. Financial Insight

10.15.5. Recent Developments

10.16. DiaSorin S.p.A.

10.16.1. Snapshot

10.16.2. Overview

10.16.3. Offerings

10.16.4. Financial Insight

10.16.5. Recent Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

List of Tables

Table 1 Types

Table 2 Study Periods

Table 3 Data Reporting Unit

Table 4 Global Next-Generation IVD Market Size, by Type, 2018-2023 (USD Billion)

Table 5 Global Next-Generation IVD Market Size, by Type, 2025-2030 (USD Billion)

Table 6 Global Next-Generation IVD Market Size, by Product Type, 2018-2023 (USD Billion)

Table 7 Global Next-Generation IVD Market Size, by Product Type, 2025-2030 (USD Billion)

Table 8 Global Next-Generation IVD Market Size, by Application, 2018-2023 (USD Billion)

Table 9 Global Next-Generation IVD Market Size, by Application, 2025-2030 (USD Billion)

Table 8 Global Next-Generation IVD Market Size, by End-use Industry, 2018-2023 (USD Billion)

Table 9 Global Next-Generation IVD Market Size, by End-use Industry, 2025-2030 (USD Billion)

Table 10 Global Next-Generation IVD Market Size, by Region, 2018-2023 (USD Billion)

Table 11 Global Next-Generation IVD Market Size, by Region, 2025-2030 (USD Billion)

Table 12 North America Next-Generation IVD Market Size, by Type, 2018-2023 (USD Billion)

Table 13 North America Next-Generation IVD Market Size, by Type, 2025-2030 (USD Billion)

Table 14 North America Next-Generation IVD Market Size, by Product Type, 2018-2023 (USD Billion)

Table 15 North America Next-Generation IVD Market Size, by Product Type, 2025-2030 (USD Billion)

Table 16 North America Next-Generation IVD Market Size, by Application, 2018-2023 (USD Billion)

Table 17 North America Next-Generation IVD Market Size, by Application, 2025-2030 (USD Billion)

Table 16 North America Next-Generation IVD Market Size, by End-use Industry, 2018-2023 (USD Billion)

Table 17 North America Next-Generation IVD Market Size, by End-use Industry, 2025-2030 (USD Billion)

Table 18 North America Next-Generation IVD Market Size, by Country, 2018-2023 (USD Billion)

Table 19 North America Next-Generation IVD Market Size, by Country, 2025-2030 (USD Billion)

Table 20 Europe Next-Generation IVD Market Size, by Type, 2018-2023 (USD Billion)

Table 21 Europe Next-Generation IVD Market Size, by Type, 2025-2030 (USD Billion)

Table 22 Europe Next-Generation IVD Market Size, by Product Type, 2018-2023 (USD Billion)

Table 23 Europe Next-Generation IVD Market Size, by Product Type, 2025-2030 (USD Billion)

Table 24 Europe Next-Generation IVD Market Size, by Application, 2018-2023 (USD Billion)

Table 25 Europe Next-Generation IVD Market Size, by Application, 2025-2030 (USD Billion)

Table 26 Europe Next-Generation IVD Market Size, by End-use Industry, 2018-2023 (USD Billion)

Table 27 Europe Next-Generation IVD Market Size, by End-use Industry, 2025-2030 (USD Billion)

Table 28 Europe Next-Generation IVD Market Size, by Country, 2018-2023 (USD Billion)

Table 29 Europe Next-Generation IVD Market Size, by Country, 2025-2030 (USD Billion)

Table 30 Asia-Pacific Next-Generation IVD Market Size, by Type, 2018-2023 (USD Billion)

Table 31 Asia-Pacific Next-Generation IVD Market Size, by Type, 2025-2030 (USD Billion)

Table 32 Asia-Pacific Next-Generation IVD Market Size, by Product Type, 2018-2023 (USD Billion)

Table 33 Asia-Pacific Next-Generation IVD Market Size, by Product Type, 2025-2030 (USD Billion)

Table 34 Asia-Pacific Next-Generation IVD Market Size, by Application, 2018-2023 (USD Billion)

Table 35 Asia-Pacific Next-Generation IVD Market Size, by Application, 2025-2030 (USD Billion)

Table 36 Asia-Pacific Next-Generation IVD Market Size, by Country, 2018-2023 (USD Billion)

Table 37 Asia-Pacific Next-Generation IVD Market Size, by Country, 2025-2030 (USD Billion)

Table 38 RoW Next-Generation IVD Market Size, by Type, 2018-2023 (USD Billion)

Table 39 RoW Next-Generation IVD Market Size, by Type, 2025-2030 (USD Billion)

Table 40 RoW Next-Generation IVD Market Size, by Product Type, 2018-2023 (USD Billion)

Table 41 RoW Next-Generation IVD Market Size, by Product Type, 2025-2030 (USD Billion)

Table 42 RoW Next-Generation IVD Market Size, by Application, 2018-2023 (USD Billion)

Table 43 RoW Next-Generation IVD Market Size, by Application, 2025-2030 (USD Billion)

Table 44 RoW Next-Generation IVD Market Size, by End-use Industry, 2018-2023 (USD Billion)

Table 45 RoW Next-Generation IVD Market Size, by End-use Industry, 2025-2030 (USD Billion)

Table 46 RoW Next-Generation IVD Market Size, by Country, 2018-2023 (USD Billion)

Table 47 RoW Next-Generation IVD Market Size, by Country, 2025-2030 (USD Billion)

Table 48 Snapshot – Abbott Laboratories

Table 49 Snapshot – Becton

Table 50 Snapshot – Dickinson and Company

Table 51 Snapshot – BioMérieux SA

Table 52 Snapshot – Bio-Rad Laboratories

Table 53 Snapshot – Danaher Corporation

Table 54 Snapshot – F. Hoffmann-La Roche Ltd.

Table 55 Snapshot – Illumina

Table 56 Snapshot – QIAGEN N.V.

Table 57 Snapshot – Shenzhen Mindray Bio-Medical Electronics Co.

Table 58 Snapshot – Siemens Healthineers

Table 59 Snapshot – Thermo Fisher Scientific Inc.

Table 60 Snapshot – Wama Diagnostica

Table 61 Snapshot – Wiener Laboratorios SAIC

Table 62 Snapshot – QuidelOrtho Corporation

Table 63 Snapshot – Agilent Technologies Inc.

Table 64 Snapshot – DiaSorin S.p.A.

List of Figures

Figure 1 Market Coverage

Figure 2 Research Phases

Figure 3 Secondary Types for Different Parameters

Figure 4 Methodology

Figure 5 Data Mining & Exploration

Figure 6 Data Triangulation

Figure 7 Assumptions for Market Estimation and Forecast

Figure 8 Market Synopsis

Figure 9 Global Next-Generation IVD Market - Growth Drivers and Restraints

Figure 10 Competitive Benchmark

Figure 11 Global Next-Generation IVD Market Highlight

Figure 12 Global Next-Generation IVD Market Size, by Type, 2018 - 2030 (USD Billion)

Figure 13 Global Next-Generation IVD Market Size, by Product Type 2018 - 2030 (USD Billion)

Figure 14 Global Next-Generation IVD Market Size, by Application 2018 - 2030 (USD Billion)

Figure 15 Global Next-Generation IVD Market Size, by End-use Industry 2018 - 2030 (USD Billion)

Figure 16 Global Next-Generation IVD Market Size, by Region, 2018 - 2030 (USD Billion)

Figure 17 North America Next-Generation IVD Market Highlight

Figure 18 North America Next-Generation IVD Market Size, by Type, 2018 - 2030 (USD Billion)

Figure 19 North America Next-Generation IVD Market Size, by Product Type 2018 - 2030 (USD Billion)

Figure 20 North America Next-Generation IVD Market Size, by Application 2018 - 2030 (USD Billion)

Figure 21 North America Next-Generation IVD Market Size, by End-use Industry 2018 - 2030 (USD Billion)

Figure 22 North America Next-Generation IVD Market Size, by Country, 2018 - 2030 (USD Billion)

Figure 23 Europe Next-Generation IVD Market Highlight

Figure 24 Europe Next-Generation IVD Market Size, by Type, 2018 - 2030 (USD Billion)

Figure 25 Europe Next-Generation IVD Market Size, by Product Type 2018 - 2030 (USD Billion)

Figure 26 Europe Next-Generation IVD Market Size, by Application 2018 - 2030 (USD Billion)

Figure 27 Europe Next-Generation IVD Market Size, by End-use Industry 2018 - 2030 (USD Billion)

Figure 28 Europe Next-Generation IVD Market Size, by Country, 2018 - 2030 (USD Billion)

Figure 29 Asia-Pacific Next-Generation IVD Market Highlight

Figure 30 Asia-Pacific Next-Generation IVD Market Size, by Type, 2018 - 2030 (USD Billion)

Figure 31 Asia-Pacific Next-Generation IVD Market Size, by Product Type 2018 - 2030 (USD Billion)

Figure 32 Asia-Pacific Next-Generation IVD Market Size, by Application 2018 - 2030 (USD Billion)

Figure 33 Asia-Pacific Next-Generation IVD Market Size, by End-use Industry 2018 - 2030 (USD Billion)

Figure 34 Asia-Pacific Next-Generation IVD Market Size, by Country, 2018 - 2030 (USD Billion)

Figure 35 RoW Next-Generation IVD Market Highlight

Figure 36 RoW Next-Generation IVD Market Size, by Type, 2018 - 2030 (USD Billion)

Figure 37 RoW Next-Generation IVD Market Size, by Product Type 2018 - 2030 (USD Billion)

Figure 38 RoW Next-Generation IVD Market Size, by Application 2018 - 2030 (USD Billion)

Figure 39 RoW Next-Generation IVD Market Size, by End-use Industry 2018 - 2030 (USD Billion)

Figure 40 RoW Next-Generation IVD Market Size, by Country, 2018 - 2030 (USD Billion)

Next-Generation IVD Market Market Coverage

Type Insight and Forecast 2025-2030

- Core Laboratory Diagnostics

- POC Testing

- Molecular Diagnostics

Product Type Insight and Forecast 2025-2030

- Consumables

- Instruments

- Software

Application Insight and Forecast 2025-2030

- Oncology/Cancer

- Infectious Diseases

- Diabetes

- Cardiology

End-use Industry Insight and Forecast 2025-2030

- Hospitals and Clinics

- Diagnostic Laboratories

- Academic and Research institutions

- Other End-Use Industries

Global Next-Generation IVD Market by Region

North America

- By Type

- By Product Type

- By Application

- By End-use Industry

- By Country – U.S., Canada, and Mexico

Europe

- By Type

- By Product Type

- By Application

- By End-use Industry

- By Country – Germany, U.K., France, Italy, Spain, Russia, and Rest of Europe

Asia-Pacific (APAC)

- By Type

- By Product Type

- By Application

- By End-use Industry

- By Country – China, Japan, India, South Korea, and Rest of Asia-Pacific

Rest of the World (RoW)

- By Type

- By Product Type

- By Application

- By End-use Industry

- By Country – Brazil, Saudi Arabia, South Africa, U.A.E., and Other Countries

Vynz Research know in your business needs, you required specific answers pertaining to the market, Hence, our experts and analyst can provide you the customized research support on your specific needs.

After the purchase of current report, you can claim certain degree of free customization within the scope of the research.

Please let us know, how we can serve you better with your specific requirements to your research needs. Vynz research promises for quick reversal for your current business requirements.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverabvle

Connect With Our Sales Team

- Toll-Free: 1 888 253 3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Next-Generation IVD Market